Table of Contents

ToggleWhy Term Insurance is Important: 7 Costly Mistakes (2026)

A ₹1 crore mistake can happen in silence when a teacher signs the wrong policy.

This is exactly why term insurance is important for teachers in India in 2026 — not as an investment, but as pure financial protection.

During a break at GHS Rang, Chowari last year, a fellow teacher leaned in and asked, “My LIC agent says this endowment plan is savings + insurance. Should I take it?”

As a school leader and personal finance writer, I replied gently: You can’t protect your family with half-baked policies. This isn’t the first time I’ve seen such confusion among salaried teachers. At Chalk2Wealth, I’ve consistently highlighted how mis-selling pushes low-cover, high-commission plans instead of real protection.

This isn’t the first time I’ve heard such confusion. At Chalk2Wealth, I’ve already shared how mis-selling traps ordinary teachers:

- In Insurance Frauds in India: How Banks Make Profits, I explained how banks and agents often push unsuitable products that generate commissions for them, not protection for you.

- And in my guide Term Life Insurance: Benefits, Myths & Is It Worth It in 2026 for Teachers?

, I broke down how a simple ₹1,000/month term plan can secure ₹1 crore cover—something no endowment or money-back plan can match.

Even the regulator IRDAI has raised red flags. In late 2024, Chairman Debasish Panda cautioned banks that “a lot of ills have crept into the system,” warning that bancassurance should remain incidental, not aggressive selling That’s why today, let’s demystify the 7 common mistakes teachers make with term insurance in 2026—and how to fix them.

For a full step-by-step buying guide, read our pillar post: Term Life Insurance: Benefits, Myths & Is It Worth It in 2026 for Teachers?

“For ₹800–₹1000/month, a government teacher can secure ₹1 crore cover.

But choosing the wrong policy can leave the family underinsured by 80%.”

Teachers, don’t let these mistakes cost your family’s future. Secure your cover today with pure term insurance.

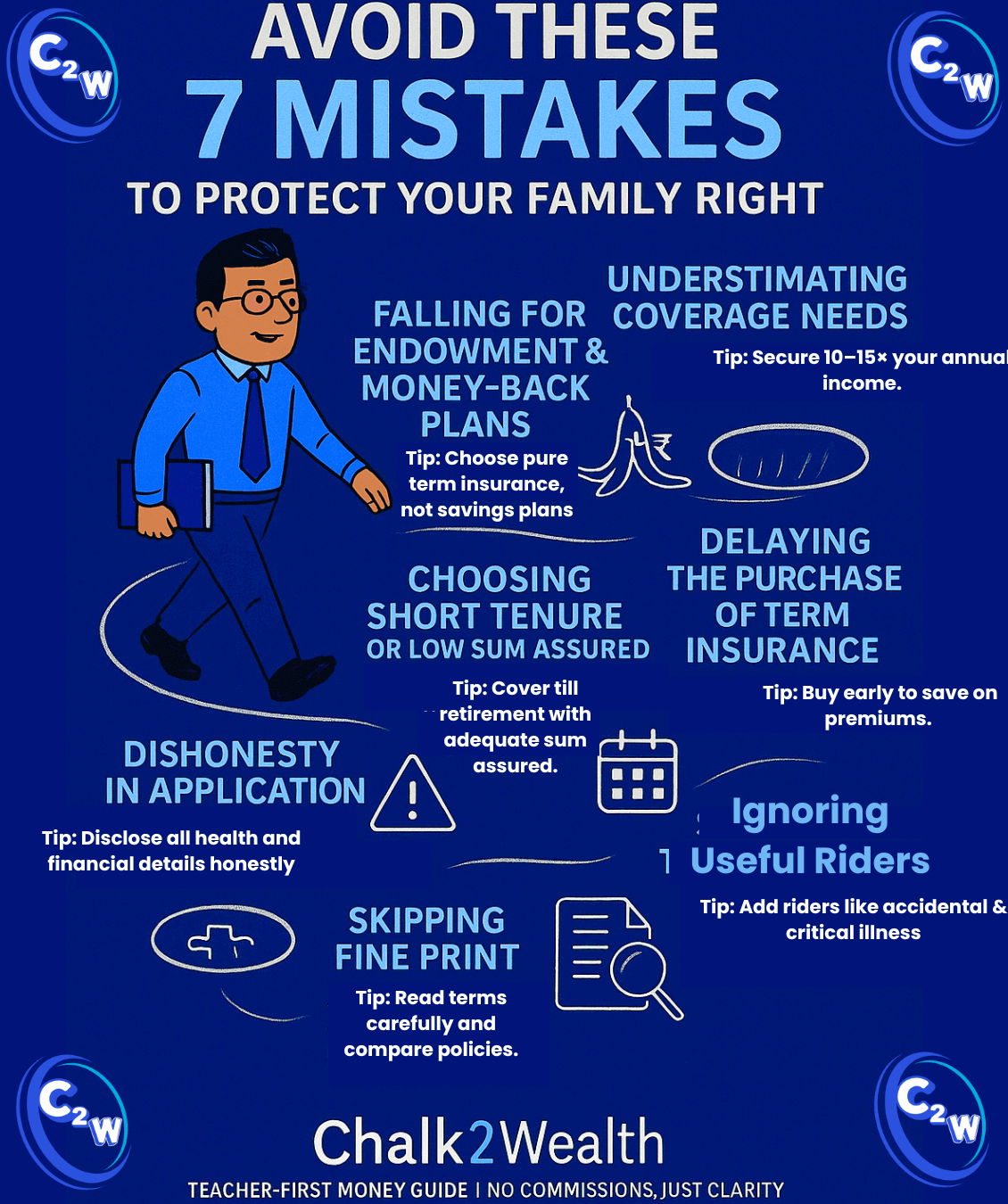

Term Insurance Mistake #1 – Choosing Too Little Coverage for Your Family

Buying a ₹25 lakh cover when your family needs ₹1 crore is like bringing an umbrella in a monsoon—useless.

- Moneycontrol advises coverage of at least 10× your annual income, adjusted for liabilities like home loans and children’s education.

- Another article suggests taking 10–15× income as a starting point for term insurance.

Teacher tip: Use an IRDAI-endorsed Human Life Value calculator (available on government portals) or combine reasonable multipliers with your liabilities to get a real figure.

Biggest Term Plan Error #2 – Confusing Insurance with Investment Plans

Endowments may sound like “insurance + investment,” but they provide low coverage at high costs.

- Term plans give 20–30× coverage for the same premium compared to endowment’s 4–5× multiple.

Teacher tip: Keep protection and investments separate. Use term insurance for cover; invest in SIPs, PPF, or Sukanya Samriddhi separately.

In our Term Life Insurance for Teachers in India 2026: Honest Guide , we break down why endowments fail teachers and how term plans solve this.

**Chalk2Wealth Note:**

IRDAI data shows mis-selling complaints were **0.41 per 100 policies in FY 2023-24**. While the number may look small, it still hurts thousands of families. This is why separating *insurance (pure term cover)* from *investment (SIPs, PPF, etc.)* is so important for teachers.

Term Policy Mistake #3 – Selecting Short Tenure to Save Small Premium

Many teachers pick a 15-year policy at 25 to save money—but this lapses just as responsibilities rise.

- Short tenure means higher future premiums and potential uninsurability.

- Moneycontrol also suggests cover lasting till your dependents are independent—often 30–40 years terms.

Teacher tip: Buy long-term while young and healthy. A ₹1 crore term policy for a healthy 30-year-old non-smoker costs around ₹700–₹900/month

Delay Cost Mistake #4 – Waiting Too Long to Buy Term Insurance

Every year you delay, premiums rise by up to 5%. On top of that, any future health issues can either increase your premium sharply or even lead to rejection of cover.

Early buyers always benefit: they lock in lower rates, enjoy wider eligibility, and secure continuous protection for their families. Remember, youth is your biggest asset when it comes to term insurance.

Teacher tip: Make term insurance a priority—even during your service probation. Don’t wait for life events to trigger purchase.

Application Mistake #5 – Hiding Health or Lifestyle Details

Some buyers try to hide smoking habits or family history to lower premiums—but most claim rejections actually stem from such misrepresentations.

Claim settlement ratios in recent years have been high, but misleading information can still put your family’s payout at risk.

Teacher tip: Always be truthful. Paying a slightly higher premium is worth the peace of mind—and ensures your family gets the protection you promised.

Protection Gap Mistake #6 – Ignoring Essential Riders in Term Plans

Riders cost a little but add a lot:

- Critical Illness Rider: Lump sum on cancer/heart ailment diagnoses.

- Accidental Death Rider: Adds extra cover for accidental demise.

- Waiver of Premium: Keeps policy active if you become disabled.

Moneycontrol confirms that such riders serve real, tangible needs with minimal premium impact.

Teacher tip: Add one or two riders that fit your personal risk profile—avoid adding every rider under the sun.

Policy Review Mistake #7 – Not Reading Fine Print or Updating Coverage

Policies often contain exclusions and waiting periods—read those. And as your life changes—marriage, child, loan—your cover should too. Experts advises reviewing coverage every 3–5 years or after major life events, and using the free-look period proactively.

Teacher tip: Use the 15-day free-look window to clarify terms. Set calendar reminders to revisit your policy regularly and update as needed.

Final Thoughts: Secure, Don’t Just Insure

IRDAI continues to caution against mis-selling via rural agents or school tie-ups. Claim settlement ratios for FY 2023-24 averaged 96.82%, yet honesty is non-negotiable for successful payouts .

To recap for teachers:

- Coverage = 10–15× annual income (adjust for liabilities).

- Choose pure term insurance—avoid endowment/money-back traps.

- Buy early, with long tenure, and honestly disclose health.

- Consider essential riders, read fine print, and review regularly.

As Chalk2Wealth reminds us, “For less than ₹1,000/month, a teacher can secure ₹50 lakh to ₹1 crore cover depending upon age factor.” That’s not spending—it’s safeguarding dedication, family, and legacy.

If you’re still deciding between different plans, go to our main guide here: Term Life Insurance: Benefits, Myths & Is It Worth It in 2026 for Teachers?

Teachers, for less than a cup of tea a day, you can secure your family’s tomorrow. Don’t delay.

FAQ: Why Term Insurance is Important

Why Term Insurance is Important ?

Term insurance is important because it provides high financial protection to your family at a low premium. In case of an untimely death, the sum assured (₹50 lakh to ₹1 crore or more) helps cover daily expenses, loans, children’s education, and long-term financial needs. Unlike endowment or money-back plans, a term plan focuses purely on protection, making it the most cost-effective way for salaried individuals and teachers in India to secure their family’s financial future and peace of mind.

Why is a Term Plan Important?

A term plan is important because it provides high life insurance coverage at an affordable premium, ensuring your family’s financial security in case of an untimely death. Unlike endowment or money-back policies, a term plan focuses purely on protection, which means you can secure ₹50 lakh to ₹1 crore cover at a much lower cost. For salaried individuals and teachers in India, a term plan helps replace lost income, repay loans, and support long-term goals like children’s education and household expenses. This is why term plan is important — it offers maximum financial protection, peace of mind, and long-term security without mixing insurance with low-return investment products.

What is the Term Insurance 3 Year Rule?

The term insurance 3 year rule means that after a policy has been active for 3 continuous years, the insurer generally cannot reject a claim due to misrepresentation or non-disclosure, except in cases of proven fraud. Under Section 45 of the Insurance Act in India, claims made after three years are more secure, provided all details were disclosed honestly at the time of purchase.

Can Term Insurance Be Rejected After 3 Years?

Yes, term insurance can still be rejected after 3 years, but only in cases of proven fraud. As per Section 45 of the Insurance Act in India, once a policy completes 3 continuous years, the insurer cannot reject a claim for minor errors or non-disclosure. However, if the company proves intentional fraud—such as hiding serious medical conditions, smoking habits, or false income details—the claim can still be denied even after 3 years.

What is the Maximum Entry Age for Term Insurance in India?

The maximum entry age for term insurance in India usually ranges between 60 to 65 years, depending on the insurer and policy type. Some insurers allow entry up to 70 years, but premiums are significantly higher and coverage options may be limited. For better affordability and longer coverage, financial experts recommend buying term insurance early (in your 20s or 30s), as it locks in lower premiums and ensures protection during peak financial responsibility years.

When Can We Claim Term Insurance?

A term insurance claim can be made after the death of the policyholder during the policy term. The nominee can file the claim immediately after the insured person’s death by submitting the death certificate, policy documents, and required claim forms to the insurer. There is no waiting period for natural or accidental death once the policy is active, except in cases like suicide, where most policies have a 12-month exclusion clause. Claims are typically settled within a few weeks if all documents and disclosures were correct.

What Are the Common Reasons for Term Insurance Claim Rejection?

Term insurance claims are usually rejected due to non-disclosure or incorrect information provided at the time of application. Common reasons include hiding medical history, smoking or alcohol habits, false income details, or not mentioning existing insurance policies. Claims may also be denied if the policy has lapsed due to unpaid premiums, death occurs during the exclusion period (such as suicide within the first 12 months), or if fraud and misrepresentation are proven. To avoid claim rejection, it is important to give honest disclosures, pay premiums on time, and carefully read the policy terms and conditions.