Table of Contents

ToggleNational Savings Certificate (NSC): How Much Should You Have in Your Investment Portfolio?

During an inspection visit, I noticed something interesting while reviewing teachers’ salary investment files — almost every teacher had Fixed Deposits. But very few had National Savings Certificates (NSC).

Not because NSC is ineffective. In fact, NSC is often overlooked despite being one of the safe investments in India with high returns for salaried individuals. The real reason is that most people were never shown how to use it strategically in a portfolio. Like every financial product, the National Savings Certificate works best when held in the right proportion, aligned with your goals, time horizon, and risk profile.

Let’s understand how to determine the right NSC allocation.

What is National Savings Certificate (NSC)?

National Savings Certificate is a Government of India-backed fixed-income investment with:

- 5-year lock-in

- Guaranteed interest (currently ~7.7% per annum)

- Section 80C tax benefits up to ₹1.5 lakh

- Reinvested annual interest qualifying again for 80C (first 4 years)

Your capital is safe, returns are predictable, and the tax advantage improves the effective yield. However, the interest is taxable at maturity. NSC is suitable for medium-term (5+ years) financial goals where capital protection and stability are priorities.

Why National Savings Certificate is Considered Among Safe Investments in India with High Returns

The National Savings Certificate offers one of the highest assured returns among small savings schemes with zero market risk. While equity and market-linked investments may deliver higher growth, NSC provides certainty — a key requirement for many salaried individuals and teachers.

This makes NSC a stable anchor inside a diversified portfolio, particularly for predictable goals over the next 5 years.

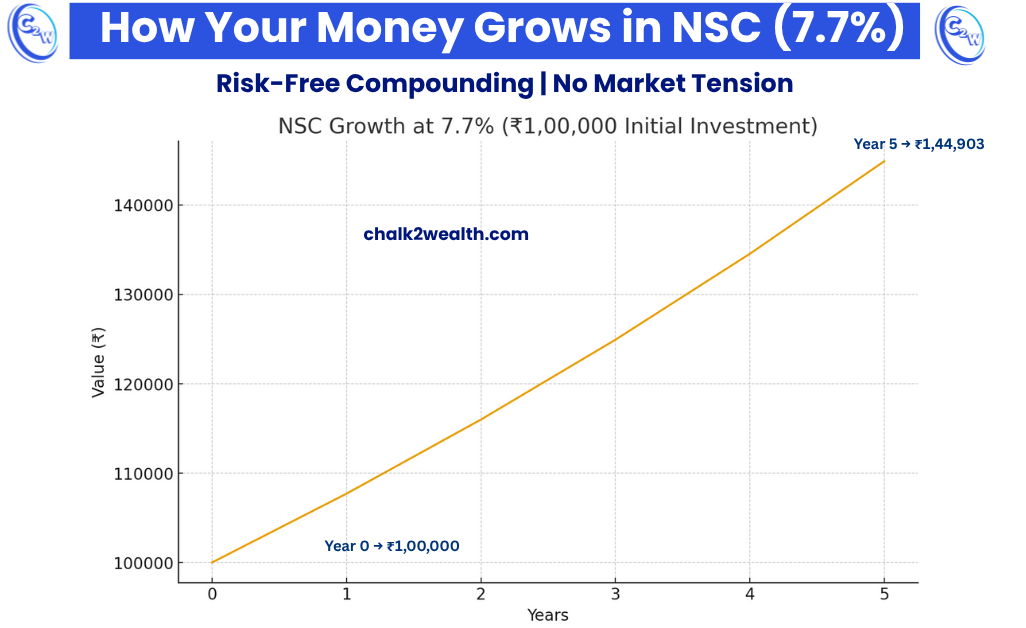

How NSC Grows — Simple Example

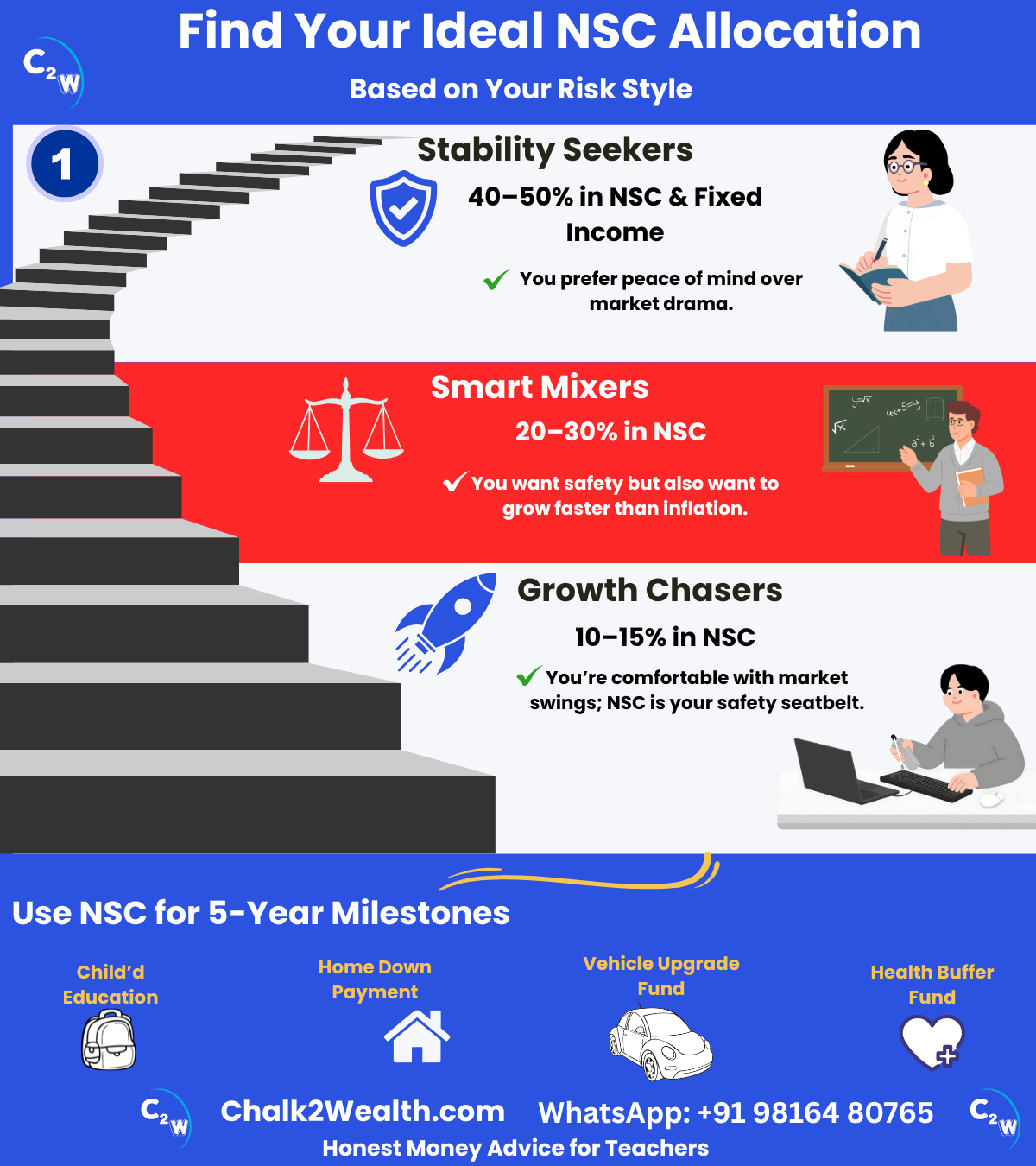

How Much of Your Portfolio Should Be in NSC?

1) Conservative Investors (Low Risk Appetite)

If your priority is capital protection (e.g., near retirement or risk-averse):

- Allocate 40–50% of your portfolio to fixed-income instruments, including NSC.

- Ensure diversification within fixed-income (NSC + PPF + Senior Citizen Scheme + FDs).

NSC forms the core stability component here.

2) Balanced/Moderate Investors

Most salaried professionals fall here — comfortable taking some market risk but still valuing safety.

- Allocate 20–30% to NSC and other assured-return instruments.

- Use NSC strategically up to the ₹1.5 lakh 80C limit for tax optimization.

This ensures:

- Capital safety for medium-term goals

- Growth through equities for long-term wealth creation

3) Aggressive Investors (High Risk Appetite)

Younger investors or those focused on long-term wealth creation may prioritize equities.

- NSC allocation: 10–15% or only enough to utilize 80C efficiently.

- The focus remains on growth-oriented instruments (e.g., equity mutual funds).

NSC acts as a capital cushion, ensuring part of your portfolio remains risk-free.

Align NSC with Goal Planning

A practical approach is to tie NSC to 5-year goals, such as:

- Child’s school/tuition expenses

- Home down payment

- Senior parent healthcare buffer fund

Match NSC maturity with the year your goal occurs, ensuring amount is available safely and predictably.

During a staffroom meeting later, I casually asked a colleague, “How much of your savings are growing safely and predictably?” She paused before responding. That pause is where thoughtful financial planning begins — not just choosing investment products, but understanding how much to allocate and why.

Conclusion: Leverage National Savings Certificate (NSC) Wisely in Your Portfolio

Conclusion: Leverage National Savings Certificate (NSC) Wisely in Your Portfolio

The National Savings Certificate is a reliable, government-backed instrument that offers:

- Predictable compounding

- Capital security

- Tax savings

Its ideal portfolio weight depends on your risk tolerance and financial timeline:

| Investor Type | Suggested NSC Allocation |

|---|---|

| Conservative | 40–50% |

| Balanced | 20–30% |

| Aggressive | 10–15% |

Used wisely, the National Savings Certificate strengthens financial stability and provides assured progress toward medium-term goals. Its predictable compounding, tax benefits, and government backing make it a dependable pillar in any portfolio. For teachers and salaried professionals, NSC stands out as one of the safe investments in India with high returns relative to risk, ensuring that a portion of your savings grows steadily while the rest of your portfolio focuses on long-term wealth creation.

National Savings Certificate (NSC) – Frequently Asked Questions

National Savings Interest Calculator: How can I estimate my NSC maturity amount?

You can estimate your NSC maturity amount by entering three details into a National Savings Interest Calculator — your investment amount, the current NSC interest rate (around 7.7% per annum), and the 5-year lock-in period. The calculator then applies annual compounding and reinvests the interest each year, showing you the exact maturity value. This helps you understand how much your National Savings Certificate will grow before you invest and allows you to plan your tax savings under Section 80C more effectively.

National Savings Certificate Interest Rates: How are NSC returns calculated over 5 years?

National Savings Certificate interest rates are fixed by the Government of India and currently stand around 7.7% per annum. NSC returns are calculated through annual compounding, where the interest earned each year is reinvested automatically. Over the 5-year lock-in period, this compounding effect boosts your maturity amount significantly. For example, at a 7.7% interest rate, ₹1,00,000 grows to roughly ₹1,44,000 at maturity. Because the rate remains fixed for the entire tenure, NSC offers predictable and stable growth.

National Savings Certificate Rates: What interest rate does NSC currently offer to investors?

National Savings Certificate rates are fixed by the Government of India and reviewed every quarter. The current NSC interest rate is around 7.7% per annum, and it remains locked for the entire 5-year tenure once you invest. This rate is compounded annually, meaning the interest earned each year is reinvested, increasing your final maturity amount. Because the rate stays constant throughout the term, NSC offers predictable and stable returns for teachers and salaried investors.

The National Saving Certificates are issued by which authority?

The National Saving Certificates are issued by the Government of India through the Department of Posts (India Post). You can purchase NSC from any post office across the country. India Post handles the certificates, interest calculation, maturity process, and record-keeping under the Small Savings Schemes regulated by the Ministry of Finance.

What is National Saving Certificate?

National Saving Certificate (NSC) is a Government of India–backed small savings scheme available through post offices. It offers a fixed interest rate, a 5-year lock-in, and tax benefits under Section 80C up to ₹1.5 lakh. NSC earns annual compounding, and the interest is reinvested automatically each year. It is considered a safe, low-risk investment option for teachers, salaried professionals, and anyone looking for predictable returns and capital protection.