Table of Contents

TogglePPF Extension Rules 2026: The Silent Mistake After 15 Years That Can Lock Your Money

A Real Moment from a Teacher’s Home

On a quiet Sunday evening, after checking notebooks and planning Monday’s classes, Meena a government school teacher opens her PPF passbook at the dining table.

“15 years complete,” it says.

There is no warning bell. No letter from the bank. Just one silent question:

What should I do now?

After 15 years, PPF doesn’t test your patience. It tests the decision you make next

This is the moment where most PPF investors feel uncertain—and where PPF extension rules suddenly become critical. Not during the first few years of investing, but right at maturity, when silence from the system forces you to decide.

The truth is, many investors don’t lose money because they chose PPF. They lose flexibility because they didn’t understand the PPF extension rules after 15 years. The decisions taken at this stage can either preserve decades of disciplined savings—or quietly lock you into limitations you never intended. (If you’re also unsure about withdrawals, this detailed guide on [PPF Rules for Withdrawal (2026): How & When You Can Withdraw Your Money Safely] will help.

PPF Extension Rules After 15-Year Maturity: What Happens Next

PPF does not mature exactly 15 years from the date you opened the account. Under the Public Provident Fund Scheme, 2019, maturity is counted as fifteen years from the end of the financial year in which the account was opened. This small detail is important, because once your PPF reaches maturity, the PPF extension rules come into play—and they give you three practical choices.

And this is exactly where most investors go wrong.

Not in the first 15 years… but on the day their PPF matures.

At the 15-year mark, you can choose one of the following paths:

- Close the account and withdraw the full amount: You may apply to close your PPF account and withdraw the entire balance. Interest is paid up to the last day of the month preceding the month of closure.

- Do nothing and retain the account without further deposits: If you take no action, the PPF extension rules allow you to continue holding the account without making new contributions. The balance continues to earn interest at the applicable rate, though withdrawals are regulated (explained below).

- Formally extend the account with fresh deposits: If you wish to continue investing, the PPF extension rules require you to opt for an extension with contributions for a fresh 5-year block. This choice must be made formally, and the implications are discussed next.

What’s New or Relevant for 2026?

For most investors, the key reassurance is this: the PPF extension rules in 2026 remain unchanged. The core post-maturity framework under the Public Provident Fund Scheme, 2019—close the account, extend it with deposits, or continue without deposits—continues exactly as before. Recent updates do not alter your maturity or extension choices. They mainly relate to

(a) how certain provisions are worded for penalties in cases of premature closure, and

(b) the quarterly notification of PPF interest rates, which is covered separately in in PPF Interest 2026: The 5th April Trick Every Teacher Must Know.

In short, if your PPF matures in 2026, you are working with the same PPF extension rules that have governed the scheme in recent years.

A simple maturity timeline to remember:

Account opened (any date in FY X) →

15-year term ends on 31 March of FY X+15 →

within one year after maturity, you must opt if you want to continue contributing.

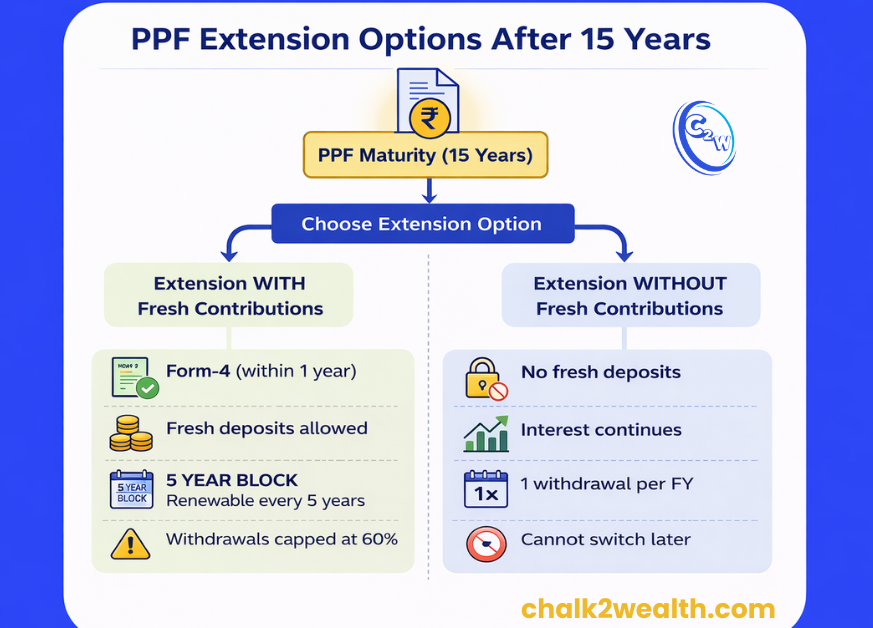

PPF Extension Options After 15 Years

After your PPF reaches maturity, the PPF extension rules give you two distinct choices. The right option depends on whether you want to keep actively investing or simply let the existing corpus grow safely.

1. Extension With Fresh Contributions

This option is meant for investors who want their PPF to continue as a long-term, low-risk, tax-efficient compounding bucket, even after the original 15-year term.

How this works under the Scheme:

- You may extend the PPF account for a further block of 5 years and continue making deposits by submitting Form-4 to the accounts office.

- A strict compliance deadline applies: the option to extend with deposits must be exercised within one year from the date of maturity.

- If this opt-in is missed and deposits are still made, the PPF extension rules are unforgiving. Any such deposit is treated as irregular and is refunded immediately without earning any interest.

- Withdrawals during this “with deposits” extension are not fully flexible. Across the 5-year block, total withdrawals are capped at 60% of the balance at the start of the block, and can be taken either as a single withdrawal or in annual instalments. (These limits are explained in detail under PPF rules for withdrawal after maturity.)

- This extension is renewable. After each completed 5-year block, the same extension-with-deposit provisions apply again.

Best suited if:

You want to keep PPF as an active savings instrument and can commit to disciplined contributions.

2. Extension Without Fresh Contributions

This is the “let it run, but stop adding money” route—often chosen by investors who have other financial priorities but still value sovereign-backed interest on an existing PPF corpus.

What the Scheme allows:

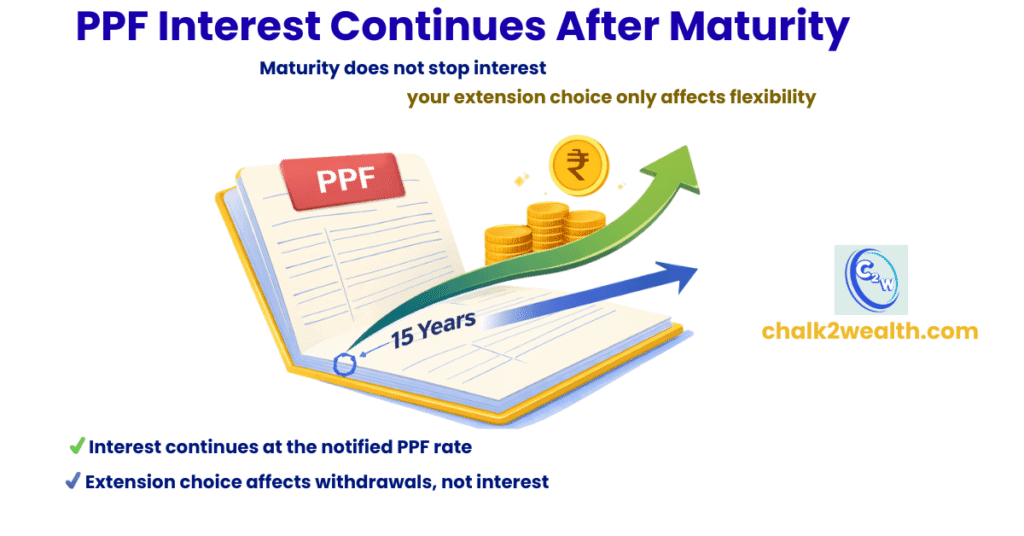

- After maturity, you may retain the PPF account indefinitely without making further deposits, and the balance continues to earn interest at the applicable rate.

- Withdrawals are permitted, but with a simple rule: only one withdrawal per financial year, for any amount within the available balance. (This is covered clearly under PPF withdrawal rules and limits in 2026.)

- A critical lock-in effect applies. Once the account is continued without deposits for more than one year, you cannot later switch back to the extension-with-deposit option.

- India Post uses a standard extension request form for PPF (and other schemes) that explicitly refers to a 5-year block period for PPF, reinforcing that extensions are processed in defined blocks and require an explicit request.

- Since many investors also worry about taxes at this stage, it’s important to note that PPF withdrawals remain tax-free, which is explained in detail in Is PPF withdrawal taxable from 2026?

Best suited if:

You want safe interest on an existing corpus without adding fresh money.

Extension Comparison: Which Option Is Better in 2026?

There is no single “best” PPF extension option for everyone. Under the PPF extension rules, the right choice in 2026 depends on one simple question:

Do you want continued tax-saving contributions and compounding, or liquidity and simplicity?

Side-by-Side Comparison

| Feature | Extend With Contributions | Extend Without Contributions |

|---|---|---|

| Can you keep adding money? | Yes — if you submit Form-4 within one year of maturity | No — deposits are not permitted |

| Withdrawal flexibility | Restricted: total withdrawals during the 5-year block are capped at 60% of the opening balance of that block | Flexible: one withdrawal per year, any amount within the balance |

| If you miss the opt-in and still deposit | Deposits become irregular and are refunded without interest | Not applicable (you are not allowed to deposit) |

| Can you later switch to “with contributions”? | Yes — only if you have not continued without deposits beyond one year | No — once continued without deposits for over a year, switching back is not allowed |

Quick Decision Rule (2026)

If you’re still unsure which option to choose, use this simple rule:

- If you want tax saving + long-term compounding → Extend with contributions

- If you want flexibility + easier withdrawals → Continue without contributions

The mistake most investors make is overthinking this decision.

In reality, it comes down to one question:

Do you want to keep investing… or start using the money?

Choose based on your goal—not habit.

How PPF Interest Is Calculated (and What Changes in 2026)

PPF interest calculation is entirely rule-based, and these rules continue to apply even during the extension period.

- Monthly interest calculation: Interest for a month is calculated on the lowest balance between the close of the 5th day and the end of that month.

- Annual crediting of interest: Although interest is calculated monthly, it is credited only at the end of the financial year, which is why PPF is commonly described as “compounded annually” in practice.

- What happens after maturity: The scheme clearly states that when a PPF account is retained after maturity—especially in the case of extension without fresh contributions—the balance continues to earn interest at the applicable PPF rate. In other words, maturity does not stop interest; your extension choice determines how flexible the account remains.

2026 Interest-Rate Update (What Investors Should Know)

For Q4 of FY 2025–26 (1 January 2026 to 31 March 2026), the Ministry of Finance announced that small savings interest rates remain unchanged from the previous quarter.

- Government reference tables have consistently shown the PPF interest rate at 7.1% in recent notifications.

- Since PPF rates are notified quarterly, investors should always verify the current quarter’s rate before making contribution or withdrawal decisions.

The key point for 2026: there is no special or separate interest rule for extended accounts—the same notified PPF rate applies.

Withdrawal Timing Nuance (Easy to Miss but Important)

One small timing detail can quietly affect your returns:

- If you close your PPF account after maturity, interest is paid only up to the last day of the month preceding the month of closure.

- This means closing the account early in a month may result in losing interest for that entire month.

For large balances, this timing decision alone can make a noticeable difference.

Common Mistakes After PPF Maturity (and How to Avoid Them)

Most post-maturity mistakes are procedural, not strategic. They usually involve missed deadlines, wrong assumptions, or timing errors.

Most PPF mistakes are not about money—they are about timing and awareness

- Missing the one-year opt-in window for extension with contributions: If you don’t opt in within one year of maturity and still deposit, those deposits are treated as irregular and refunded without interest. This is one of the most common errors highlighted in Investing in PPF: 8 Smart Things to Know Before You Start.

Action: Set a reminder and submit the extension request well before the deadline.

- Assuming you can switch later from “without contributions” to “with contributions” : The Scheme does not allow this once the account is continued without deposits for more than a year. If there’s any chance you may want to keep investing, choose with contributions early.

- Misunderstanding withdrawal limits in extension with contributions: Total withdrawals during a 5-year block are capped at 60% of the opening balance. These limits often surprise investors at the wrong time and are explained clearly under PPF Rules for Withdrawal (2026): How & When You Can Withdraw Your Money Safely.

Action: Plan large expenses in advance, or choose the without-contributions option if liquidity matters.

- Poor deposit timing within a month : Deposits made after the 5th of the month usually don’t earn interest for that month. This small timing error can quietly reduce returns, as explained in PPF Interest 2026: The 5th April Trick Every Teacher Must Know.

Action: Deposit on or before the 5th whenever possible.

Seema’s PPF matures on 31 March 2026 with a balance of about ₹28 lakh. She wants long-term safety but also needs money for a home renovation in 2027–28.

- With contributions: allows continued investing, but withdrawals are capped.

- Without contributions: no new deposits, but one flexible withdrawal each year.

She chooses without contributions for flexibility, while setting a reminder to reassess within one year—before losing the option to switch.

Conclusion

For PPF investors in 2026, maturity should be treated as a clear decision point with a deadline, not as an automatic continuation. First, confirm your exact maturity date—15 years from the end of the financial year in which the account was opened. Then make a conscious choice: close the account, extend it with deposits (by submitting Form-4 within one year), or continue without deposits.

What matters most is awareness of consequences. Missing the opt-in window and still depositing can lead to refunds without interest, while remaining in the “without deposits” mode for too long can permanently block your ability to switch back to contributions. A timely, informed decision ensures your years of disciplined saving continue to work exactly as you intend.

Before you act: confirm maturity date → decide extension type → submit Form-4 (if needed) → set a 1-year reminder

Remember PPF doesn’t make you rich in 15 years. It reveals how you think about money when it finally matters.

Disclaimer:

This article is for informational and educational purposes only. PPF rules are subject to change. Please verify details with official government notifications, your bank, or post office before making any financial decisions.

PPF Extension Rules: Frequently Asked Questions

How to extend PPF account?

You can extend your PPF account after 15 years by submitting Form H at your bank or post office within one year of maturity if you want to continue making deposits. If you do not submit Form H, the PPF account is automatically extended without contribution, meaning no fresh deposits are allowed but interest continues to be earned.

PPF account extension rules – what should an investor do after PPF maturity?

Under PPF account extension rules, after 15 years you must submit Form H within one year of maturity if you want to extend the account with contribution and continue deposits. If Form H is not submitted, the PPF account is automatically extended without contribution, where interest continues but no fresh deposits are allowed.

PPF withdrawal rules after extension – how much money can you withdraw?

Under PPF withdrawal rules after extension, withdrawals depend on the type of extension chosen. If the PPF account is extended without contribution, you can withdraw any amount at any time during the extension period. If the account is extended with contribution (Form H submitted), withdrawals are limited to up to 60% of the balance available at the start of the 5-year extension block, and this can be withdrawn in one or multiple installments.

PPF extension limit – how many times can a PPF account be extended?

There is no maximum limit on PPF extension. A PPF account can be extended indefinitely in blocks of 5 years after the initial 15-year maturity. However, if you want to extend the PPF account with contribution, you must submit Form H within one year of maturity at the start of each 5-year extension block.