Table of Contents

TogglePPF Loan vs PPF Withdrawal: Which Is Better & When to Choose Each?

Last Friday, Mr. Arvind, a salaried professional, walked into his bank with a familiar dilemma. He was finalising a small residential property but needed quick cash. His PPF had a healthy balance—yet he wasn’t sure: should he take a PPF loan or make a PPF withdrawal? This confusion is common among salaried professionals and teachers when big expenses demand liquidity without damaging long-term savings or violating PPF withdrawal rules (explained in detail in this guide on PPF Rules for Withdrawal (2026): How & When You Can Withdraw.

PPF Loan vs PPF Withdrawal: What Is the Core Difference?

A PPF loan allows you to borrow against your Public Provident Fund balance to meet short-term financial needs during the early years of the account. Under the Public Provident Fund Scheme, 2019, the loan amount cannot exceed 25% of the balance available at the end of the second year preceding the year of application. The loan must be repaid within 36 months, and the interest charged is 1% higher than the prevailing PPF interest rate.

A PPF withdrawal refers to money taken out from your PPF account as permitted under PPF rules. Partial withdrawal is allowed only after the completion of five years from the end of the financial year in which the account was opened and is limited by a prescribed formula linked to past account balances. Full withdrawal is permitted on account closure after maturity—15 years from the end of the year of opening—or in cases of allowed premature closure under PPF rules.For investors who choose not to close the account at maturity, understanding the PPF Extension Rules 2026: What Investors Should Do After 15-Year Maturity becomes critical to avoid withdrawal restrictions and loss of flexibility.

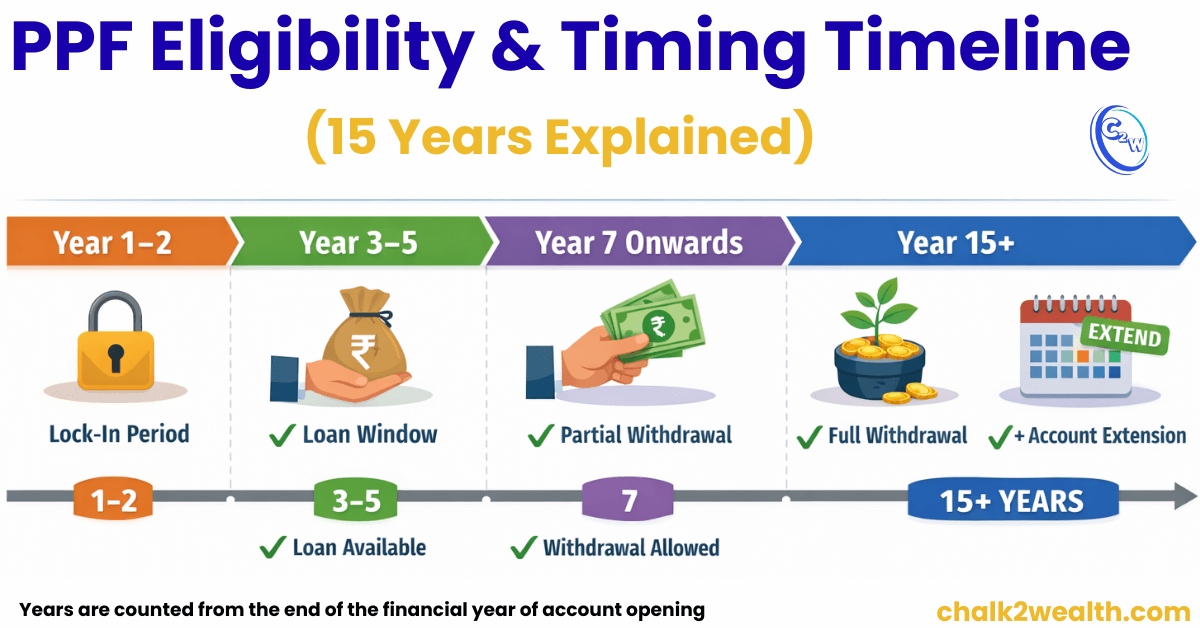

Eligibility & Timing Rules

Loan: As per the official PPF Scheme rules issued by NSI India, a PPF loan is allowed from the 3rd financial year to the end of the 5th financial year from the year of opening the account (that is, after one year from the end of the year of first subscription and before five years from that year-end). Only one loan may be taken in a financial year, and no fresh loan is permitted until the earlier loan is fully repaid. This facility is available only for regular (non-discontinued) PPF accounts.

Withdrawal: Partial withdrawal from a PPF account is allowed after the completion of five years from the end of the financial year in which the account was opened (that is, from the 7th financial year onwards). Only one withdrawal is permitted per financial year, and the amount is restricted to the eligible balance as per prescribed rules. Any outstanding PPF loan along with interest must be fully repaid before a withdrawal can be made.

PPF Loan vs PPF Withdrawal: Key Differences You Should Know

| PPF Loan | PPF Withdrawal | |

|---|---|---|

| When | 3rd–5th FY from year of opening | 7th FY onward (partial); after maturity (full) |

| Amount | ≤25% of balance at end of 2nd FY preceding | ≤50% of eligible balance (prescribed formula) |

| Cost | 1% p.a. above PPF rate (penal interest if delayed) | No cost; reduces compounding base |

| Repayment | Principal within 36 months | No repayment; loan + interest must be cleared first |

| Frequency | One loan per FY | One partial withdrawal per FY |

| Tax | Not income (not taxable) | Exempt under Section 10(11) |

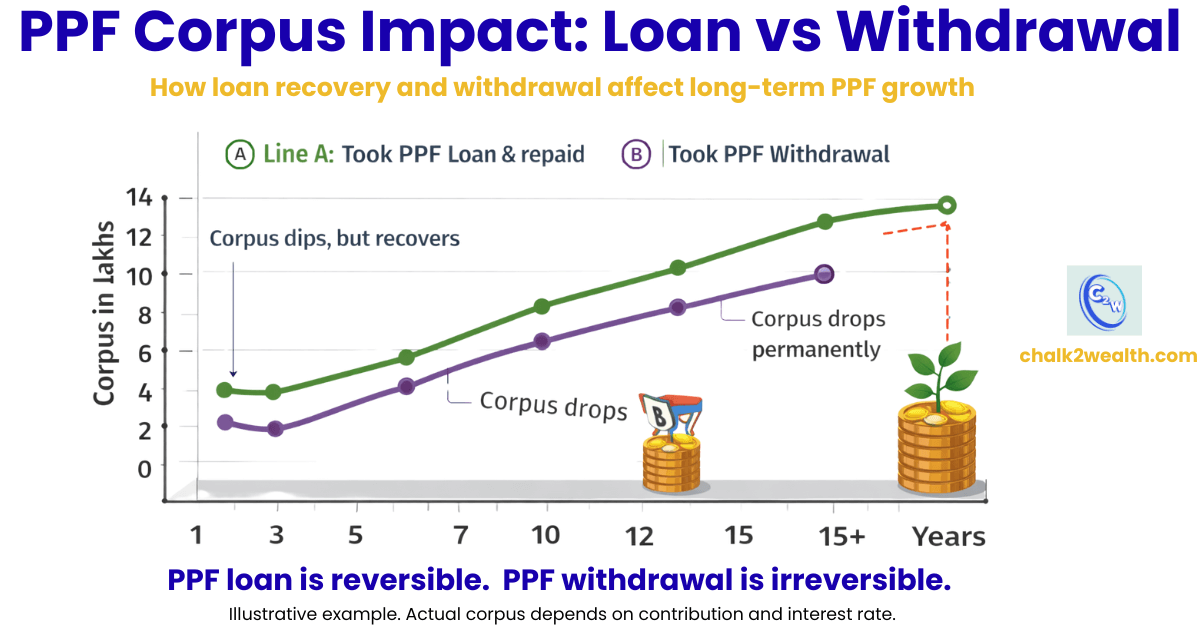

A loan is reversible; a withdrawal is irreversible

As per PPF guidelines by the National Savings Institute, a PPF loan is a reversible liquidity option (you repay and your corpus recovers). A PPF withdrawal is irreversible (no repayment, but your compounding base drops). So, loan fits short-term needs with repayment capacity; withdrawal fits later-stage planned expenses where you want zero repayment pressure.

Interest & Repayment Impact

PPF interest is calculated monthly on the lowest balance between the 5th day and the last day of each month and is credited annually. The Government notifies PPF interest rates periodically under the small-savings framework. PPF interest is calculated monthly (on the lowest balance between the 5th and month-end) and credited annually. A PPF loan must be repaid within 36 months, with interest charged at PPF rate + 1% (penal interest applies if delayed). A withdrawal has no cost, but permanently reduces your interest-earning balance.

Tax Treatment: Loan vs Withdrawal

PPF withdrawals made in accordance with the scheme are fully tax-exempt, as payments received from a Central Government–notified provident fund are exempt under Section 10(11) of the Income Tax Act. In addition, PPF contributions are eligible for deduction under Section 80C, subject to the overall annual limit of ₹1.5 lakh.

A PPF loan, on the other hand, is not treated as taxable income because it is a repayable liability, not a receipt or gain. Since the loan amount must be repaid along with interest, it does not create any tax liability at the time of receipt.

When to Choose PPF Loan or PPF Withdrawal (and Mistakes to Avoid)

Choose a PPF loan when you need short-term emergency liquidity during the eligible early years of your PPF account and have the capacity to repay comfortably from regular salary income. This option suits teachers and salaried professionals with predictable monthly cash flows. It works well for urgent needs such as medical expenses or unexpected travel, as it provides funds without permanently reducing the PPF corpus, provided the loan is repaid on time. Since repayment must be completed within 36 months and delays attract penal interest, a PPF loan should be chosen only if you have a clear repayment plan and confidence that EMIs will not be missed.

Choose PPF withdrawal when you are eligible and the expense is planned or large, such as higher education fees, home renovation, or debt reduction, where avoiding repayment pressure is important. Partial withdrawals are restricted under PPF rules—generally allowed once per financial year and capped at 50% of the eligible balance as per the prescribed formula. If there is an outstanding PPF loan, it must be fully repaid along with interest before any withdrawal is allowed. After maturity (15 years from the end of the opening year), the account can be closed and the entire balance withdrawn, making withdrawal the natural option for long-term goals or retirement needs.

Common mistakes to avoid include applying for a PPF loan outside the eligible early-year window, taking a second loan before repaying the first, or missing the 36-month repayment deadline, which leads to penal interest. For withdrawals, many investors misunderstand that the five-year lock-in is counted from the end of the opening financial year, not from the date of deposit, and that partial withdrawal is typically allowed only once per year. Another frequent oversight is allowing the account to become discontinued, which can block loan or partial withdrawal facilities until the account is regularised—one of the important PPF rules many investors miss when investing for the long term.

Final Verdict for Salaried & Teachers

For salaried professionals and teachers, a PPF loan is best suited for early-tenure emergencies when you have the ability to repay comfortably within 36 months from regular salary income. It provides short-term liquidity without permanently reducing the PPF corpus, as long as repayments are made on time.

A PPF withdrawal is the better choice in the later years of the account for planned or larger expenses, especially when taking on repayment obligations would strain monthly budgets. Since withdrawals permanently reduce the amount earning PPF interest, they should be used thoughtfully and preferably for long-term goals.

To preserve PPF tax benefits and keep both options available, ensure the account remains regular by making the minimum annual contribution and strictly follow the eligibility and timing rules—key principles every investor should understand when investing in PPF.

If your need is <3 years → loan; if one-time & final → withdrawal.