Table of Contents

TogglePPF vs Fixed Deposit: Which Is Better for Teachers After Tax?

Every staffroom has one heated debate — not about students, but savings.

It was lunchtime in the staffroom when Mr.Sunil Sharma, a senior science teacher, brought up a familiar dilemma. “My FD is maturing next month,” he said, stirring his tea. “But someone told me PPF gives better returns after tax.”

Instantly, the discussion began.

“FDs are safer and more flexible,” argued Mr. Vijay from the Math department. “But PPF is tax-free and perfect for retirement,” chimed in Miss Gupta, who had recently opened her own account. She also mentioned that before investing, understanding withdrawal rules is important, especially in long-term schemes like PPF (read: PPF Rules for Withdrawal (2026): How & When You Can Withdraw Your Money Safely).By the end of the break, the debate was still unresolved — and Mr. Sharma looked more confused than ever.

This isn’t just his story — thousands of teachers face the same question every year: PPF vs Fixed Deposit — which one is actually better after tax? Both options are trusted and low-risk, but they serve different financial goals. In this post, let’s simplify the comparison to help you make the right choice for your future.

PPF vs Fixed Deposit: What Should Teachers Choose After Tax?

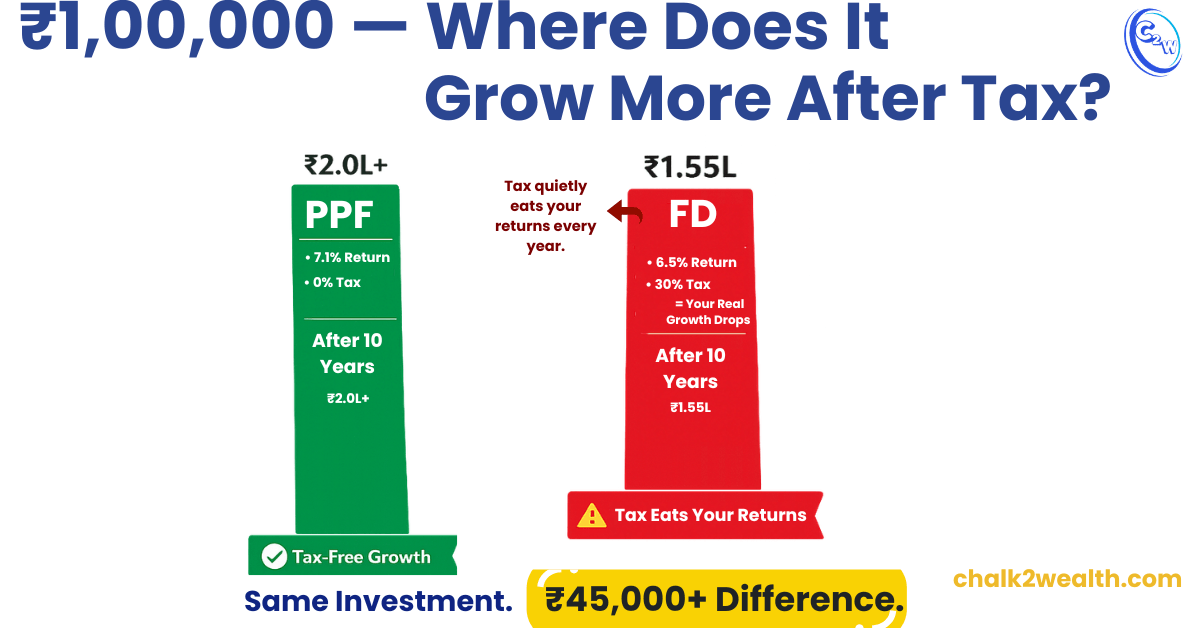

Most government teachers also contribute to pension funds, so long-term planning matters. PPF is a 15-year government-backed savings scheme that pays about 7.1% per year (current rate).

Under Section 80C of the Income Tax Act, PPF contributions up to ₹1.5 lakh qualify for deduction, making it especially relevant for salaried teachers. Its big advantage: interest is completely tax-free (EEE).

By contrast, bank FDs let you pick a term from 6 months up to 10 years. Top banks today offer roughly 6–6.5% p.a. on multi-year FDs (for regular citizens). However, that interest is fully taxable. At a 30% tax rate, a 6.5% FD yield becomes only about 4.6% effective.

Note: Returns are illustrative. Actual FD returns depend on your tax slab and prevailing interest rates.

| Factor | PPF | FD |

|---|---|---|

| Safety | Sovereign-backed | Bank-backed |

| Lock-in | 15 years (long-term) | 6 months – 10 years |

| Liquidity | Low (long-term lock-in) | High (can withdraw anytime) |

| Tax on interest | Nil (EEE) | Fully taxable |

| Post-tax return (30% slab) | ~7% | ~4.5–5% |

| Inflation protection | Medium | Low |

Conclusion: PPF vs Fixed Deposit

When it comes to PPF vs Fixed Deposit, teachers planning for a safe and tax-efficient retirement should lean toward PPF. Its long-term lock-in may seem rigid, but the tax-free interest and government backing make it a focused choice for building a retirement nest egg. If you need access to your money in the next 1–3 years, a Fixed Deposit can serve short-term needs — just remember that returns are fully taxable and may not beat inflation.

For long-term goals, avoid putting all your savings into FDs. In the PPF vs Fixed Deposit debate, PPF clearly wins for retirement-focused financial planning.

- Choose PPF if you’re a government teacher planning for retirement It aligns with long-term goals, offers tax-free returns, and protects your savings from unnecessary erosion over time.

- Choose FD if you need access to your money within 2–3 years FDs are useful for short-term goals like vacations, emergency funds, or school fees — just be mindful of the tax bite.

Don’t use FD as your long-term retirement tool

Even if it feels “safe,” FD returns are taxed — and inflation will reduce their real value. For anything beyond 5 years, PPF is a smarter, more tax-efficient choice.