Table of Contents

ToggleWhich Term Insurance Is Good in India? Teacher’s Checklist (2026)

Last week in the staffroom, Sunita madam asked Abhishek sir, “Which term insurance is good in India? I just want something safe for my family.”

Abhishek replied honestly, “Everyone talks about low premium and high claim settlement ratio, but how do we know which term insurance is good for teachers like us?” He added, “Before choosing, it also helps to understand the basic difference between protection plans and savings-based policies, like in this guide on Term Insurance vs Endowment Plan: Which Saves More Money for Teachers?, so we don’t mix insurance with investment by mistake.”

If you’re also searching which term insurance is good, you’re not alone. Most salaried teachers look for one thing — maximum financial protection with minimum risk and a smooth claim process for their family. Instead of getting distracted by marketing terms like “cheapest plan” or “best term insurance plan in India,” a safer approach is to first understand what pure term life cover actually offers, as explained in Term Life Insurance: Benefits, Myths & Is It Worth It for Teachers?, and then evaluate insurer reliability and policy clarity. This teacher’s checklist focuses on how to choose term insurance using practical factors that actually matter at the time of claim — such as insurer service record, policy clarity, and consumer-focused standards aligned with India’s insurance regulations and IRDAI guidelines.

Which Term Insurance Is Good? What “Good” Really Means in 2026

A simple way to understand which term insurance is good is this: it should be a pure-risk life cover that provides adequate protection for your dependents, remains affordable throughout the premium-paying term, and is issued by a well-regulated insurer. If you’re still unsure what pure term cover actually means, it helps to first understand the basics of term life insurance, including common myths and real benefits, before comparing plans.

To reduce fine-print surprises, insurers now provide a Customer Information Sheet (CIS) under life insurance guidelines as mandated under Insurance Regulatory and Development Authority of India policyholder disclosure norms. This sheet clearly summarises key details like policy type, sum assured, benefits, exclusions, free-look period, and claim and grievance process—helping you know exactly what you bought without struggling with complex legal jargon.

Regulatory Signals That Show an Insurer Is Reliable

Solvency Ratio: If you’re evaluating which term insurance is good, solvency ratio is a key reliability signal. Solvency reflects an insurer’s ability to meet its long-term claim obligations. As per regulatory norms highlighted in official financial disclosures and parliamentary references, insurers are required to maintain a solvency margin above the control level (generally 150% of the Required Solvency Margin). In simple terms, a higher solvency ratio indicates stronger financial capacity to pay claims over time, which is crucial for long-duration term plans.

Claims Outcomes (Not Just Claim Settlement Ratio): Many buyers judge insurers only by the headline Claim Settlement Ratio (CSR), but that alone does not show the full picture. Regulatory disclosures available in official IRDAI annual reports provide a detailed breakdown of death claims into categories such as paid, repudiated, rejected, unclaimed, and pending. This broader view helps you assess real claim experience, possible documentation issues, and underwriting strictness. So, when deciding which term insurance is good, look beyond CSR and focus on overall claim outcomes and consistency in claim servicing.

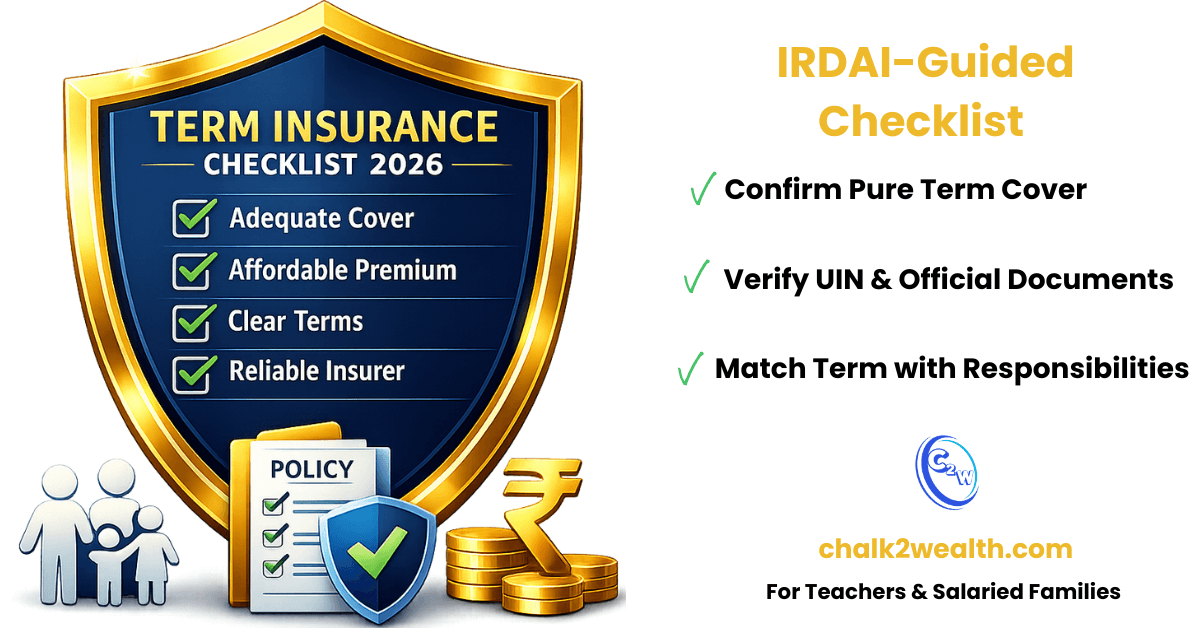

Teacher’s Checklist for 2026

Use this practical checklist when deciding which term insurance is good for your family. Keep two tabs open: the product’s Customer Information Sheet (CIS) or policy wording, and the insurer’s latest regulatory disclosures (like annual reports or handbooks).

- Confirm it is pure term cover (protection-first): The CIS should clearly mention the policy type as term insurance. Avoid mixing up protection with “returns” products.

- Verify UIN and official documents: A genuine policy will have a Unique Identification Number (UIN), and the CIS will state that policy wording prevails. If documents are unclear, do not rush the purchase.

- Match policy term to real responsibilities: Align the policy term and premium-paying term with key financial duties like children’s education, home loan tenure, and income replacement period.To select a suitable sum assured based on your salary, dependents, and long-term obligations, it is also helpful to review a practical guide on how much term insurance a teacher may need before finalising coverage.

- Test premium affordability: A good plan is one whose premium you can comfortably pay even in a financially difficult year. A lapsed policy offers zero protection.

- Choose riders only for real risks: Add riders like disability or critical illness only if they fill a genuine protection gap and remain within your budget. Always read exclusions carefully.

- Use the free-look period wisely: Life insurance policies come with a 30-day free-look window after receiving the policy document, allowing you to review terms and cancel if unsuitable.

- Understand claim timelines (inform your nominee): Policyholder-protection guidelines specify defined timelines for claim processing in normal cases, with interest implications if delays occur beyond prescribed limits.

- Check grievance and complaint system: Insurers are required to maintain formal grievance redressal mechanisms and integrate complaint tracking with official platforms like Bima Bharosa for transparency.

- Know the Ombudsman support: If disputes remain unresolved, the Insurance Ombudsman framework provides an independent escalation channel, and insurers are required to act on Ombudsman awards within stipulated timelines.

This checklist keeps the focus on clarity, affordability, and claim readiness — the three factors that truly define which term insurance is good for risk-averse teachers and salaried families in 2026.

How to Compare Plans Without Getting Misled (and Common Mistakes to Avoid)

When evaluating which term insurance is good, begin with a clean comparison based on reliability, clarity, and long-term suitability — not just premium. Shortlist insurers only after checking core regulatory signals like solvency (around the 150% / 1.50 control level), IRDAI-reported death-claim outcomes, and whether the Customer Information Sheet (CIS) and policy wording clearly explain benefits, exclusions, policy term, premium schedule, and the claim and grievance process.

Next, compare the real “fit” factors: adequate sum assured, policy term flexibility, premium-paying term, and rider costs. A plan that looks cheapest on premium but lacks clarity, service consistency, or transparent documentation may not be a good plan in practice.

A common mistake when asking which term insurance is good is treating “low premium” as the only decision factor. Other avoidable errors include skipping the free-look review and giving incomplete or inaccurate disclosures in the proposal form, which can create claim complications later. A careful comparison with full disclosure and document review leads to better long-term protection for your family.

Conclusion

So, which term insurance is good in 2026? It is the one that clears a simple, practical checklist: adequate life cover for your dependants, a premium you can sustain for the full term, clear CIS and policy wording, a financially sound insurer meeting solvency norms, and a transparent, time-bound claim and grievance process.

Instead of chasing labels like “the best term insurance plan in India,” focus on reliability, clarity, and long-term affordability. A plan that looks cheapest on premium but lacks clarity, service consistency, or transparent documentation may not be a good plan in practice. Many teachers also get confused between protection and savings-based policies, which is why understanding the difference explained in Term Insurance vs Endowment Plan: Which Saves More Money for Teachers? can help you avoid choosing the wrong product.

FAQ: which term insurance is good

Which term insurance is best in India?

There is no single “best” term insurance plan in India for everyone. The best plan is the one that offers adequate life cover, affordable long-term premium, clear policy wording (CIS), and comes from a financially strong insurer with good claim servicing record. Instead of choosing only on low premium or brand name, compare factors like solvency ratio (minimum 1.5 or 150% as mandated by IRDAI), claim outcomes, policy term flexibility, and transparency in benefits and exclusions

Which life insurance is good?

A good life insurance policy is one that matches your goal. If your priority is family protection, a term insurance plan is generally considered good because it offers high life cover at an affordable premium. The right policy should provide adequate sum assured, clear policy terms, and come from a financially reliable insurer with a consistent claim record, rather than just being the cheapest option.

Which term plan is good?

A good term plan is one that gives high life cover at an affordable premium, comes from a financially strong and well-regulated insurer, and has clear policy terms (benefits, exclusions, and claim process). Instead of choosing only the cheapest plan, compare factors like claim settlement record, solvency strength, policy clarity (CIS), and long-term affordability, because the real purpose of term insurance is to provide reliable financial protection to your dependants at a low cos

How much term insurance do I need?

A practical rule is to take term insurance cover of at least 10–15 times your annual income, plus any outstanding loans and future financial responsibilities (like children’s education). For salaried professionals and teachers, the goal is simple: the sum assured should be enough to replace your income and support your family’s expenses for many years if you are not there. Avoid choosing low cover just to save premium — adequate protection is more important than the cheapest plan.

Why is term insurance important?

Term insurance is important because it provides financial protection to your family if something happens to you during the policy term. It replaces lost income, helps repay loans, and supports major future expenses like children’s education and household needs. Since it offers high life cover at a relatively low premium, term insurance ensures your dependants remain financially secure without burdening them during an already difficult time.

How many term insurance policies can I have?

You can have multiple term insurance policies in India; there is no legal limit on the number of term plans you can buy. However, the total coverage you are eligible for depends on your income, existing liabilities, and financial profile. Insurers assess your total sum assured across all policies during underwriting, so you must disclose all existing life insurance plans honestly in the proposal form. Having multiple policies can help increase overall coverage or diversify across insurers, but the key is that the total cover should be reasonable and affordable based on your income