Table of Contents

TogglePPF Interest vs Inflation: Is Your Money Still Growing in 2026-27?

Last week in the staffroom, a colleague asked me a question about PPF interest.

“Sir, PPF interest is around 7.1%… but prices of everything are rising. Is my money actually growing?”

It’s a very important question. The Public Provident Fund (PPF) is one of the most trusted long-term savings schemes in India. Many teachers and salaried professionals rely on PPF interest to build a safe retirement corpus or fund their children’s education. If you want to track your savings regularly, here is a simple guide on how to check your PPF balance online in SBI, Post Office, and other banks.

But here is the real issue most investors ignore. It is not enough to know the PPF interest rate. What truly matters is whether PPF interest is higher than inflation, because only then does your real purchasing power grow over time.

In this guide, we will break down PPF interest vs inflation and see whether your money is actually growing.

Current PPF Interest Rate (FY 2026–27)

As of 5 March 2026, the PPF interest rate is 7.1% per year, according to the official Government small-savings scheme table. This PPF interest rate is not fixed permanently. The government reviews small-savings rates every quarter.

These reviews usually take effect on:

- 1 April

- 1 July

- 1 October

- 1 January

So while the PPF interest rate currently stands at 7.1%, it can change in future depending on government policy and economic conditions.

Apart from the interest rate, PPF is structured as a long-term disciplined savings scheme:

- Minimum yearly investment: ₹500

- Maximum yearly investment: ₹1,50,000

- Lock-in period: 15 years.

- Extension option: 5-year blocks after maturity

Because of its government backing, tax benefits, and steady PPF interest, many teachers and salaried professionals consider PPF a core component of long-term financial planning.

However, many investors still wonder whether PPF is better than market-linked options like SIPs. If you want a detailed comparison, read this guide on PPF vs SIP in 2026 for teachers and salaried professionals.

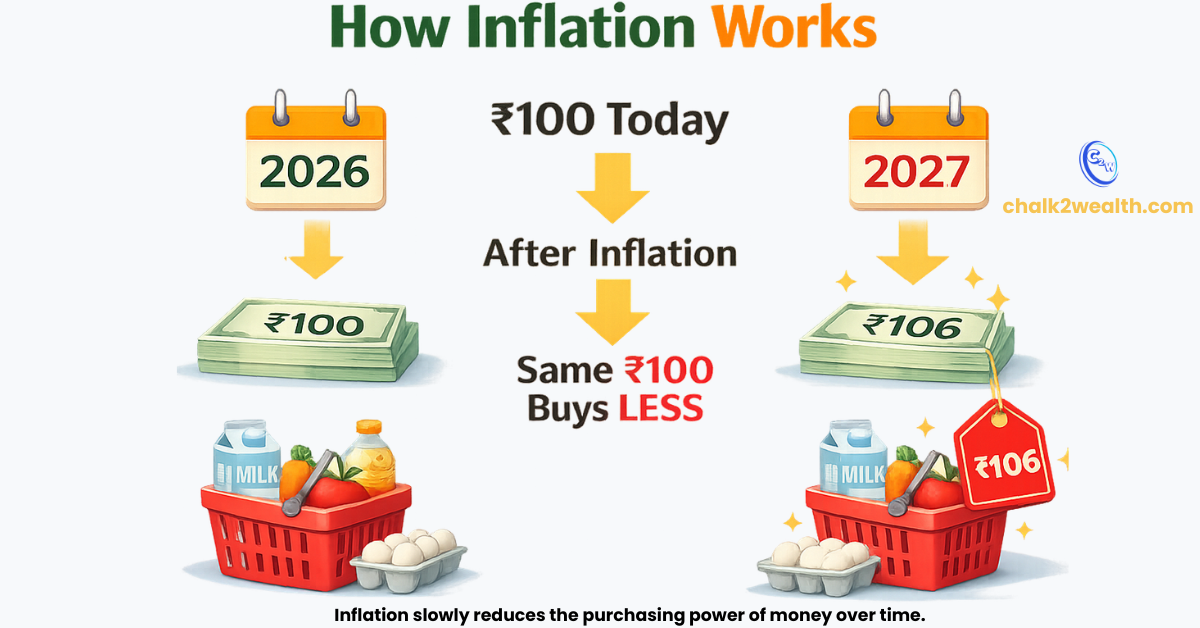

What is Inflation?

Inflation simply means the rise in prices of everyday goods and services over time. When inflation increases, the purchasing power of money falls. For example, if something costs ₹100 today and inflation is around 6%, the same item may cost about ₹106 next year. This means the same ₹100 will buy fewer goods than before.

In India, inflation is commonly measured through the Consumer Price Index (CPI). The Reserve Bank of India (RBI) regularly tracks CPI inflation to understand how prices are changing across the economy.

This is why inflation matters when evaluating PPF interest. If PPF interest is higher than inflation, your money grows in real terms. But if inflation rises faster than PPF interest, the purchasing power of your savings may slowly decline.If you want to understand whether PPF alone is enough for long-term wealth creation, you can also read this detailed comparison of PPF vs SIP in 2026 for teachers and salaried professionals.

PPF Interest vs Inflation Comparison

To understand whether PPF interest actually grows your money, we need to compare the PPF interest rate with inflation. If the PPF interest rate is higher than inflation, your savings grow in real terms. If inflation rises faster, your purchasing power declines.

Below is a comparison of PPF interest (7.1%) with India’s CPI inflation (combined) for recent financial years.

| Financial Year | PPF Interest Rate (%) | CPI Inflation (%) | Real Return (PPF − Inflation) (%) |

|---|---|---|---|

| 2020–21 | 7.1 | 6.2 | 0.9 |

| 2021–22 | 7.1 | 5.5 | 1.6 |

| 2022–23 | 7.1 | 6.7 | 0.4 |

| 2023–24 | 7.1 | 5.4 | 1.7 |

| 2024–25 | 7.1 | 4.6 | 2.5 |

What the Data Shows

Looking at the table, PPF interest has remained stable at 7.1% since April 2020, while inflation has fluctuated between about 4.6% and 6.7%. This means PPF has generally delivered a positive real return, although the margin has sometimes been small.

For example:

- In 2022–23, inflation was 6.7%, so the real return from PPF was only 0.4%.

- In 2024–25, inflation dropped to 4.6%, increasing the real return to about 2.5%.

So while PPF interest usually manages to beat inflation slightly, it does not create very high real returns. Instead, PPF works best as a safe, stable long-term savings instrument rather than a high-growth investment. If you want to see how PPF compares with market-linked investments that may offer higher long-term growth, read our detailed guide on PPF vs SIP in 2026 for teachers and salaried professionals.

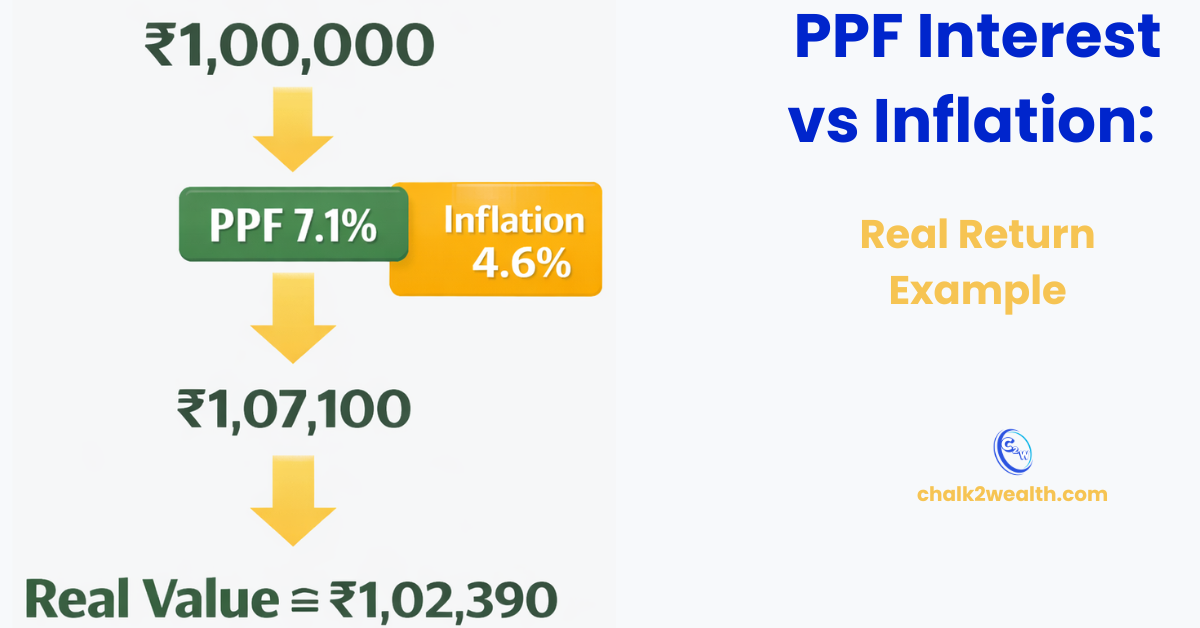

Example: How Inflation Affects Your PPF Returns

Let’s take a simple example. Suppose you invest ₹1,00,000 in PPF for one year and the PPF interest rate is 7.1%.

After one year, your money becomes: ₹1,00,000 → ₹1,07,100

Now assume inflation during the same year is 4.6%.

Because prices have risen, the real purchasing power of ₹1,07,100 is not the same as before. In today’s terms, its value is roughly ₹1,02,390.

So the real gain after adjusting for inflation is about:

₹2,390 (around 2.4%)

This example shows an important idea:

Even though PPF interest is 7.1%, the real return after inflation may be closer to 2–3%. This is why comparing PPF interest vs inflation is essential for understanding how your money actually grows.

When PPF Beats Inflation

PPF interest generally delivers positive real returns when inflation stays moderate.

For example, if the PPF interest rate is around 7% and inflation stays near 4–5%, investors may earn a real return of about 2–3%.

For a low-risk government-backed instrument, this level of real return is considered quite reasonable. That is why many conservative savers use PPF as a stable long-term savings tool.

Limitations of PPF

Despite its stability, PPF also has some limitations.

- Interest rate changes: The PPF interest rate is reviewed quarterly, so it may increase or decrease depending on government policy.

- Long lock-in period: he standard tenure is 15 years, although extensions in 5-year blocks are allowed. This makes PPF unsuitable for short-term financial goals. However, investors should also understand the official PPF withdrawal rules and conditions before investing for the long term.

- Inflation risk: Even if PPF interest is credited safely, high inflation can reduce the real return of your savings.

Advantages of PPF Despite Inflation

Even with inflation concerns, PPF remains attractive for many investors.

Key advantages include:

- Government-backed safety

- Encourages disciplined long-term saving

- Extension allowed in 5-year blocks : After the 15-year maturity period, investors can extend their PPF account in additional 5-year blocks to continue earning tax-free interest. You can read the detailed rules in this guide on PPF Extension Rules 2026: What Investors Should Do After 15-Year Maturity.

- Tax benefits under Section 80C

Because of these features, PPF interest is often considered one of the safest long-term returns available to Indian investors.

PPF vs Other Safe Investments

When comparing safe investment options, it is important to understand how returns are generated.

- Bank Fixed Deposits (FDs) – returns depend on the interest rate declared by the bank.

- Sovereign Gold Bonds (SGBs) – returns depend largely on gold price movement.

- National Pension System (NPS) – market-linked, so returns can fluctuate.

PPF, on the other hand, falls into the administered-rate category, where the government sets the interest rate periodically. This makes it a low-volatility and stable investment option. However, investors who are willing to take some market risk often compare PPF with equity-based investments like SIPs. You can read a detailed comparison in this guide on PPF vs SIP in 2026 for teachers and salaried professionals.

Should Teachers Still Invest in PPF?

For teachers and salaried professionals who value safety and discipline, the answer is generally yes.

PPF works best as a long-term savings bucket:

- Minimum investment: ₹500 per year

- Maximum investment: ₹1,50,000 per year

- Standard tenure: 15 years

For retirement planning, PPF can serve as the stable foundation of a savings plan, while other investments can provide additional growth.

Tips to Beat Inflation

A practical strategy is “PPF + diversification.”

This means:

- Use PPF for safe, long-term compounding

- Maintain an emergency fund

- Add growth-oriented investments for long-term goals (10–20 years) such as mutual fund SIPs. You can read a detailed comparison in this guide on PPF vs SIP in 2026 for teachers and salaried professionals.

This balanced approach helps ensure that your overall financial plan stays ahead of inflation while maintaining stability.

Conclusion

So, does PPF interest still grow your money in FY 2026–27?

The answer depends largely on inflation. When inflation remains moderate, PPF interest has historically delivered a positive real return. But when inflation rises sharply, the real gain can become quite small.

For teachers and conservative investors, PPF remains a strong and reliable foundation for long-term savings. However, relying only on PPF may not be enough if your goal is to consistently beat inflation over the long term.