Table of Contents

ToggleWhy Term Insurance Delay by 5 Years Can Quietly Cost You Lakhs in 2026

At 48, Rohit stares at his phone again:

₹35,000 debited. Annual term insurance premium.

He sighs.

“Every year I pay this… and get nothing back. Sometimes I wonder why I even took it.”

No returns.

No maturity value.

Just money going out.

It’s a question many quietly carry:

Is term insurance really worth it if there’s no return?

(You can explore this deeper here → Is Term Insurance Worth It? The 2026 Truth Insurance Agents Won’t Tell You)

Then Rohit pauses.

“Last year, a colleague passed away. Same age. No warning.”

Silence.

“Within months, his family started struggling—EMIs, school fees, daily expenses.”

He looks up, this time differently.

That’s when the real purpose of term insurance becomes clear — pure protection, not returns. (If you’re still unsure what a term plan actually is, read → What Is the Term Plan? 2026 Guide for Teachers (Benefits & Myths)

“That’s when I understood why term insurance exists.”

“It’s not about returns. It’s about making sure your family doesn’t struggle if you’re not there.”

And suddenly…

₹35,000 doesn’t feel like a loss anymore.

It feels like the one decision protecting everything he’s built.

Quick Answer: Why Term Insurance Matters

Term insurance matters because it replaces your income if something happens to you—ensuring your family can continue their life without financial struggle.

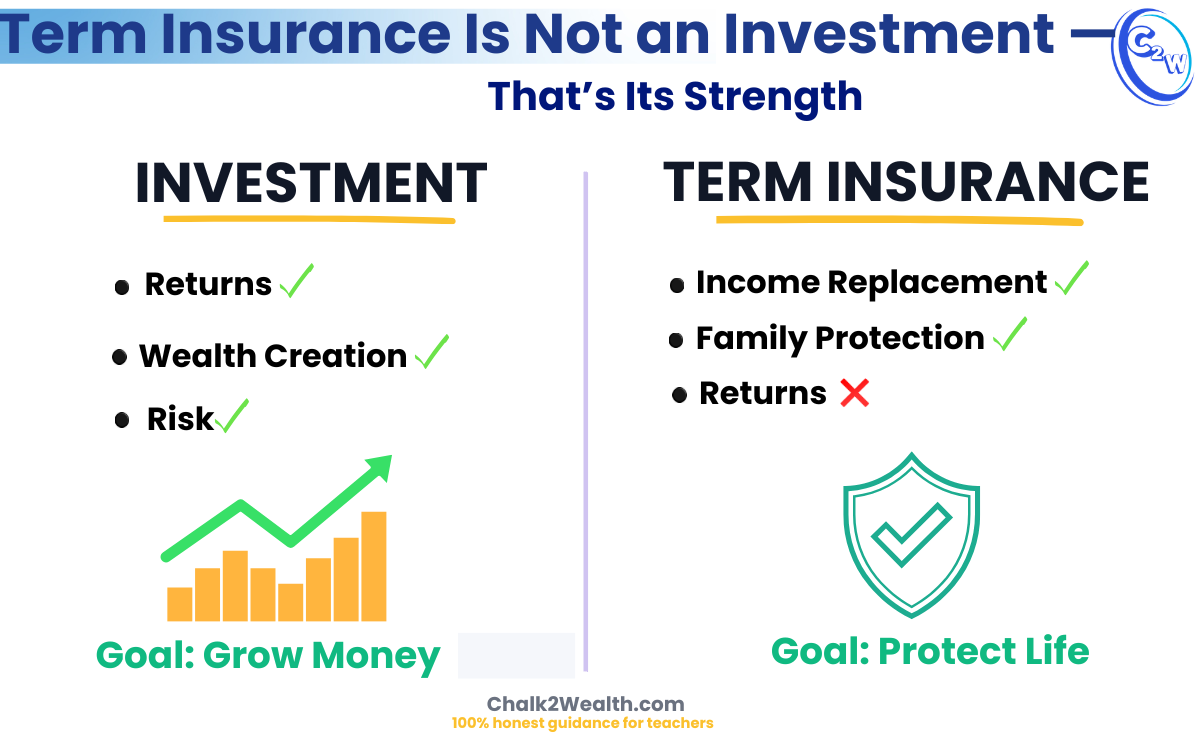

Why Term Insurance Isn’t an Investment—It’s Your Family’s Only Income If You’re Not There

Most people look at insurance like an investment.

That’s the mistake.

Term insurance is not designed to give returns—it’s designed to replace your income.

(Still confused about this? Read → Is Term Insurance Worth It? The 2026 Truth Insurance Agents Won’t Tell You)

The real reason why term insurance matters is simple:

It replaces your income when you’re gone.

- If death occurs → your family gets the sum assured

- If you survive → no payout

No confusion. No dual purpose. And that’s exactly why it works.

Maximum protection. Minimum cost.

(If you’re wondering how much protection is enough → How Much Term Insurance Do I Need as a Teacher in 2026?)

People often compare:

- Term Insurance (no returns)

- Endowment / ULIP (returns + insurance)

But here’s the reality:

Mixing insurance + investment = expensive and inefficient

(See real comparison → Term Insurance vs Endowment Plan: Which Saves More Money for Teachers in 2026?)

Think of term insurance like this:

“If I’m not there, my income should still continue.”

That’s it.

Not returns.

Not maturity value.

Not wealth creation.

Just protection.

(If you’re still at the beginner stage → What Is the Term Plan? 2026 Guide for Teachers (Benefits & Myths)

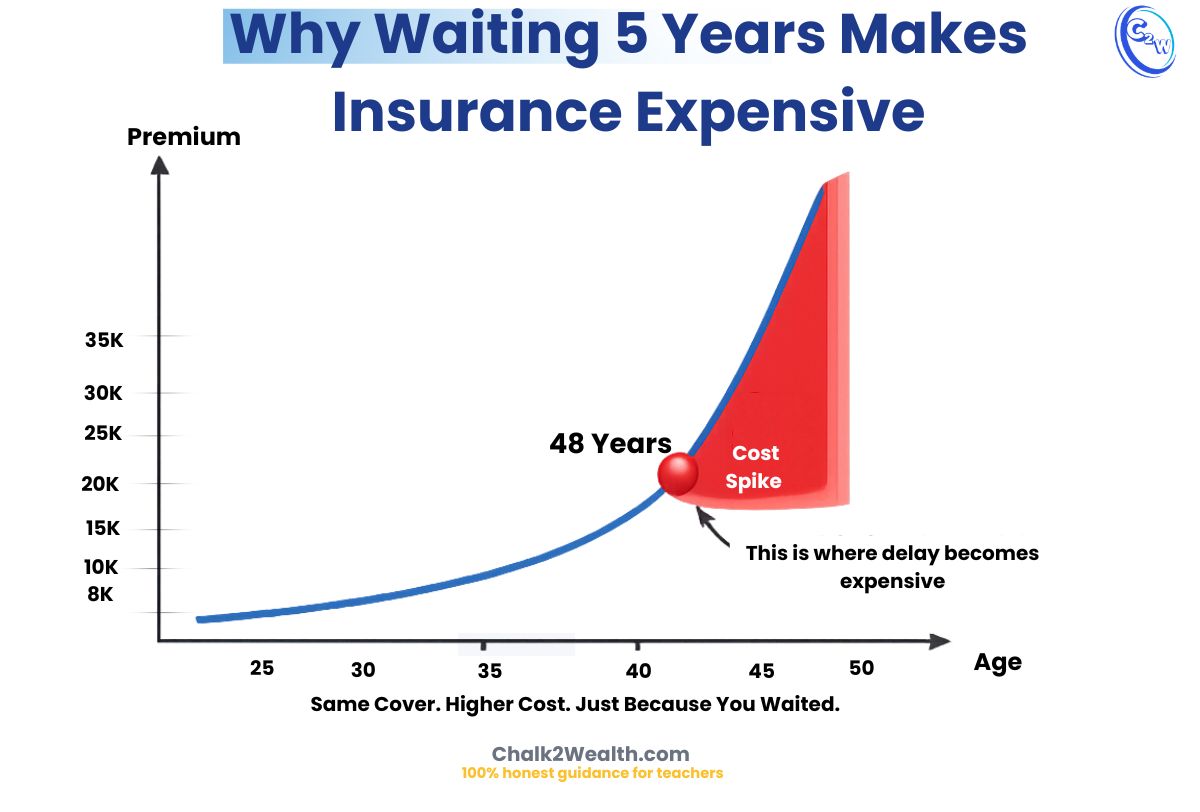

Term Insurance Delay: The Real Cost of Waiting

If Rohit had bought at 43 instead of 48, the difference wouldn’t be small.

It would be significant over time.

Here’s the simple rule:

Risk increases with age → Premium increases with age

- 40 → manageable

- 45 → noticeable jump

- 50 → sharp rise

Across major insurers, ₹1 crore cover premiums rise steeply in your 40s. A 5-year delay doesn’t just increase premium— it creates a long-term financial penalty

The Second Shock: Health Changes the Equation

In your late 40s, reality shifts:

- BP

- Sugar

- Cholesterol

And suddenly:

- Premium gets loaded

- Policy may be postponed

- In some cases, even rejected

This is the risk people ignore when delaying.

The Hidden Cost Nobody Calculates

There’s one loss you can never recover: Years without protection

From 43 to 48:

- No cover

- No backup

- No safety net

If something happens during this period: Your family gets ₹0

While expenses don’t stop:

- EMIs continue

- School fees continue

- Daily life continues

What a 5-Year Delay Really Costs: ₹3 Lakh + No Protection

Before looking at the numbers, understand this:

- These are not random assumptions.

- These are based on typical premium ranges from leading Indian insurers in 2026 (for healthy non-smokers).

(₹1 crore cover, healthy non-smoker, 25-year term):

| Age | Annual Premium | Total Cost |

|---|---|---|

| 43 | ~₹34,000 | ~₹8.5 lakh |

| 48 | ~₹46,000 | ~₹11.5 lakh |

Same person. Same cover. Same term. Only difference? 5 years delay.

Difference: ₹12,000/year

Over 25 years: ₹12,000 × 25 = ₹3,00,000 extra

That’s the visible cost.

But the invisible cost? 5 years with zero protection

Premium difference costs lakhs… but being uninsured can cost everything.

Why Term Insurance Matters: Income Protection, Not Returns

Most people keep asking the wrong question:

“What will I get back?”

But once you truly understand why term insurance matters, everything becomes brutally clear:

It’s not about getting money back It’s about protecting your family’s income

The Truth Most People Realize Too Late

- It’s about starting early, when cost is lowest

- It’s about locking protection before health becomes a problem

Delay makes it expensive

Waiting increases risk

Time is the biggest factor

The Shift That Changes Everything

People chase “cheap premium”…

But that’s the wrong goal.

Because the real objective is: Family continuity—even when your income stops

Term insurance isn’t about returns. It’s about making sure your family’s life doesn’t collapse when yours stops.

Why Term Insurance Isn’t Optional for Most Families

If you’re still thinking about why term insurance, don’t overcomplicate it—just check your situation:

- You have dependents → Term insurance is NOT optional

- You have loans (EMIs) → Term insurance is a MUST

- You earn monthly income → You NEED income protection

If none of the above applies → You may delay (but never ignore completely)

Final Verdict: The Risk Most People Realize Too Late

Here’s the uncomfortable truth behind why term insurance matters:

- Income stops, expenses don’t

- Savings are never enough for long-term survival

- One mistake = years of family struggle

Most people think the mistake is buying late.

But the real mistake?+ Staying unprotected while life is still uncertain

You can earn money again…

but your family can’t earn you back.

Before You Delay Further, Ask Yourself This:

- If something happens tomorrow…

- Will your family’s income continue?

- Or will everything depend on savings that may not last?

- If you’re still unsure whether this decision is worth it, read this honestly: Is Term Insurance Worth It? The 2026 Truth Insurance Agents Won’t Tell You

- If you’re planning to take action, start with clarity: How Much Term Insurance Do I Need as a Teacher in 2026?

- And before you buy anything, avoid the mistakes that cost families the most: Why Term Insurance Claims Get Rejected and How Teachers Can Avoid It

Term insurance doesn’t give you returns. It gives your family time, stability, and dignity when you’re not there.