Table of Contents

ToggleIs Term Insurance Worth It? The 2026 Truth Insurance Agents Won’t Tell You

Last month in the staffroom, a colleague asked me:

“If term insurance has no maturity benefit… is it even worth it?”

In simple words, he was asking what many people search online:

Is term insurance worth it in India in 2026?

Instead of answering, I asked him one question:

“If something happens to you tomorrow, how long can your family survive without your income?”

Silence.

Because here’s the uncomfortable truth:

For around ₹900 per month, you can secure ₹1 crore for your family. Yet most people ignore it—simply because there are no “returns.”

That’s the mistake.

Term insurance is not an investment. It is a financial backup your family cannot create after you’re gone.

In simple terms, a term plan pays your nominee a lump sum if you die during the policy term. If you survive the term, there is usually no payout.

If you’re still unclear about how term plans actually work, read this detailed guide:

What Is the Term Plan? 2026 Guide for Teachers (Benefits & Myths)

So the real question isn’t about returns.

Many people compare term insurance with traditional plans that offer maturity benefits. If you’re confused between the two, this comparison will help:

Term Insurance vs Endowment Plan: Which Saves More Money for Teachers in 2026?

The real question is this:

If something happens to you tomorrow, how long could your family manage without your income?

That is what “worth it” truly means in personal finance.

In this guide, we’ll clearly answer is term insurance worth it for teachers and salaried professionals in India in 2026.

Quick Answer: Is Term Insurance Worth It in 2026?

Yes — term insurance is absolutely worth it for most salaried professionals in India.

For a small monthly cost, it provides a large financial safety net that can protect your family’s income for years. While it does not offer maturity returns, its real value lies in ensuring your family does not struggle financially in your absence.

Think of it this way:

- You are not buying returns

- You are buying financial certainty for your family

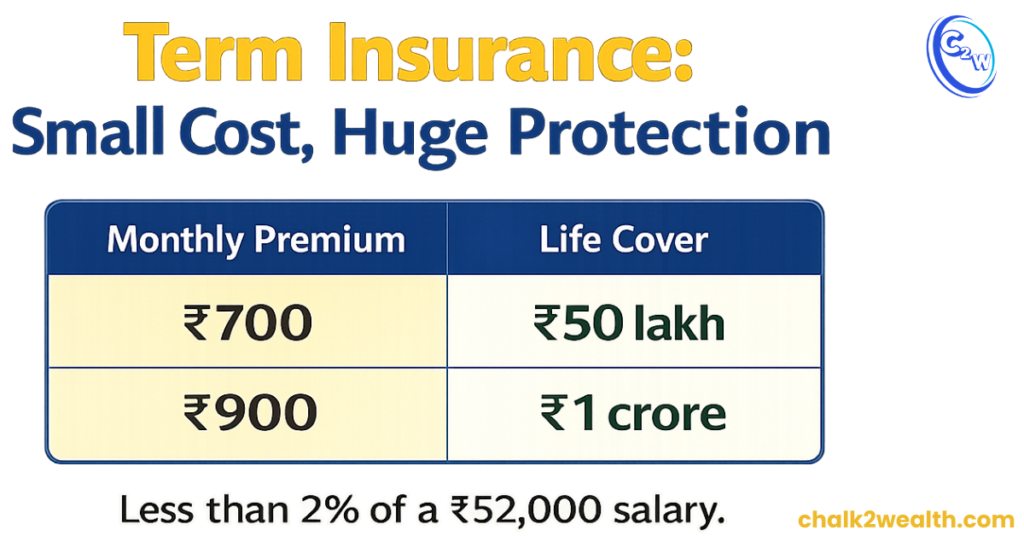

For example, a healthy individual may get ₹50 lakh to ₹1 crore life cover for roughly ₹700–₹900 per month (actual premiums vary by age, health, and insurer).

That’s often less than 2% of a monthly salary — but it can replace 10–15 years of income for your family.

As per guidelines from Insurance Regulatory and Development Authority of India, it is important to disclose accurate personal and health details while purchasing a policy to ensure smooth claim settlement.

In simple terms:

If your family depends on your income, term insurance is not optional — it is essential.

Disclaimer: Premium amounts and coverage shown are illustrative examples. Actual term insurance premiums depend on age, health profile, policy term, and insurer.

Cost vs Coverage: Is Term Insurance Worth It for a Typical Teacher?

Disclaimer: Figures are illustrative. Actual premiums and coverage may vary by insurer, age, and health profile.

Let’s look at a realistic example.

Imagine a teacher earning ₹45,000–₹60,000 per month. Assume the monthly salary is ₹52,000.

A simple household budget might look like this:

- House rent / home expenses: ₹15,000

- Groceries: ₹8,000

- Loan EMIs: ₹10,000

- Utilities + transport: ₹6,000

- Family support and other needs: ₹5,000

That already totals ₹44,000 per month.

Now imagine what happens if that income suddenly stops. Within a few months, the household budget could come under serious pressure. This is where the real question arises: is term insurance worth it for a salaried professional?

Public online illustrations suggest that a 30-year-old healthy non-smoker may pay roughly ₹700–₹900 per month for substantial coverage, depending on the insurer and policy terms.

For example:

- Around ₹50 lakh cover may cost about ₹700 per month.

- Around ₹1 crore cover may cost roughly ₹800–₹900 per month.

Premiums vary depending on age, health profile, and insurer, so actual prices may differ. Always compare multiple policies before buying. If you’re unsure how much coverage you actually need based on your income, read this detailed guide:

How Much Term Insurance Do I Need as a Teacher in 2026?

Even at ₹900 per month, that is only about 1.7% of a ₹52,000 salary.

For the cost of a few small monthly expenses, a family could receive financial protection worth many years of income But choosing the right insurer and policy features is equally important. Use this checklist before buying: Which Term Insurance Is Good in India? Teacher’s Checklist (2026)

In other words, for less than 2% of a teacher’s monthly salary, a family could receive protection worth 15–20 years of income.

And if you’re still comparing term insurance with return-based plans, this breakdown will help you decide clearly:

Term Insurance vs Endowment Plan: Which Saves More Money for Teachers in 2026?

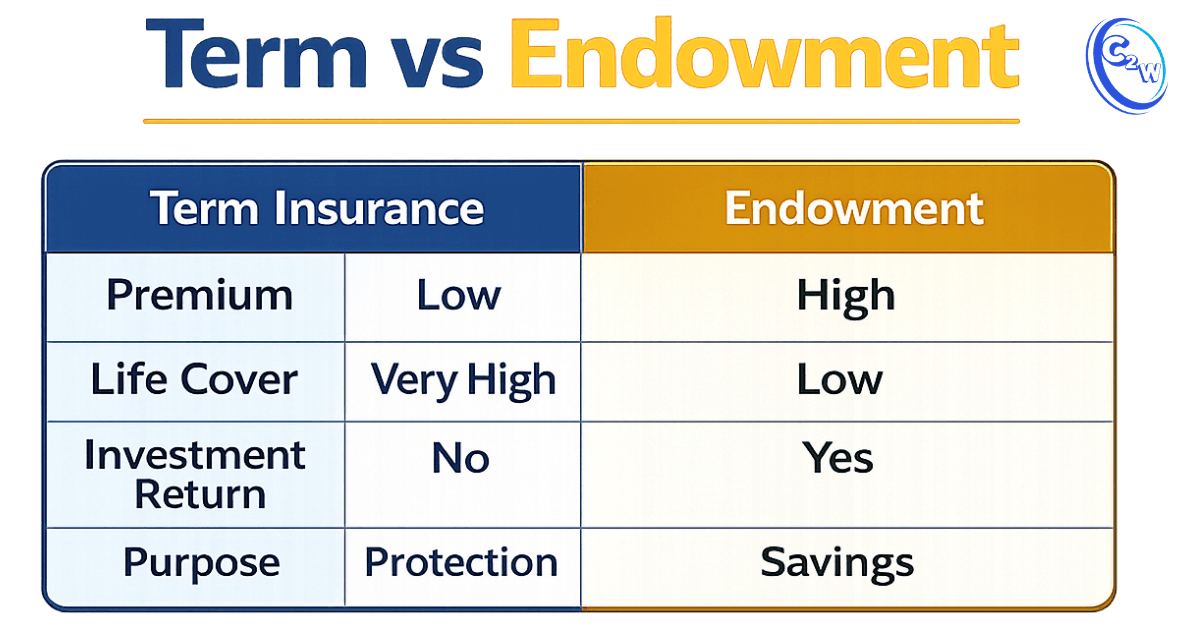

Term Insurance vs Endowment: Which Is Worth It?

| Feature | Term | Endowment |

|---|---|---|

| Cost | Low | High |

| Cover | High | Low |

| Return | No | Low |

| Purpose | Protection | Mixed |

Endowment feels safe. Term actually protects

To answer the question “is term insurance worth it?”, it helps to compare it with a traditional alternative: endowment policies.

Term insurance is pure protection. It provides life cover for a fixed period and pays your nominee a lump sum if you die during the policy term (and sometimes in case of disability). If you survive the term, there is usually no maturity payout.

An endowment policy, on the other hand, combines insurance and savings. It pays a benefit on death, and it also pays a maturity amount if you survive the policy term.

This is where many investors get confused.

Endowment plans can feel “safe” because you see a guaranteed maturity value. However, the premium is much higher compared to term insurance. As a result, many salaried families end up buying low life cover just to keep premiums affordable — which defeats the main purpose of insurance: protecting the family’s financial future.

For a detailed breakdown, read our guide on term insurance vs endowment plans.

When Term Insurance Is NOT Worth It

Although term insurance is valuable for many families, there are situations where it may not be necessary.

1. No financial dependents: If no one depends on your income, term insurance may be optional. For example, a single person with no spouse, children, or loans that would fall on parents may not need large life cover. Before deciding, it’s important to understand the real purpose of term insurance: What Is the Term Plan? 2026 Guide for Teachers (Benefits & Myths)

2. You are already financially independent: If you already have sufficient assets or savings to clear debts and support your family’s living costs, additional life cover may not add much financial value. In such cases, your investments themselves act as financial protection.

3. Very late entry or serious health conditions: If someone applies for term insurance at an older age or with major health issues, premiums can become expensive and policy approval may be difficult. In such cases, choosing the right insurer and understanding policy conditions becomes critical: Which Term Insurance Is Good in India? Teacher’s Checklist (2026)

In such situations, it may be wiser to first focus on:

- Reducing liabilities

- Building an emergency fund

- Strengthening long-term savings

Term insurance works best when purchased early, while premiums are low and eligibility is easier.

Final Verdict: Is Term Insurance Worth It for Teachers in 2026?

For most teachers and salaried professionals who have parents, a spouse, children, or a home loan, term insurance is usually worth it. The cost-to-coverage ratio is difficult to match with any other financial product. For many families, the answer to “is term insurance worth it” becomes clear when they think about the financial security of the people who depend on them.

The key is to use it correctly: buy enough cover to protect your dependents and keep your investments separate from insurance. Also, fill the proposal form carefully. Official consumer guidance warns that incorrect or incomplete disclosures can lead to claim rejection.

If you ever feel that a policy was mis-sold, you can file a complaint through the National Government Services Portal , which routes insurance complaints through IRDAI’s Integrated Grievance Management System and allows you to track the status online.

Reader Note

The examples in this article are simplified for illustration. Insurance premiums vary depending on age, health, insurer, and policy features. Always read the policy document carefully and compare multiple insurers before making a decision.

FAQ: is term insurance worth

Is term insurance good for salaried professionals in India?

Yes, term insurance is generally considered a good financial protection tool for salaried professionals in India. It provides a large life cover at a very low premium compared to traditional insurance plans. If the policyholder passes away during the policy term, the nominee receives the sum assured, which can help the family manage expenses, repay loans, and maintain financial stability. However, term insurance does not offer maturity benefits, so it should be viewed purely as protection rather than an investment.

Is term insurance necessary for salaried professionals?

Term insurance is not legally required, but it is considered financially necessary for most salaried professionals who have family responsibilities. It provides a large life cover at a very affordable premium, ensuring that dependents can manage household expenses, repay loans, and maintain financial stability if the earning member is no longer there. For individuals with dependents, such as a spouse, children, or aging parents, term insurance acts as a financial safety net and is often one of the most important protection tools in a personal finance plan.

Is term insurance tax benefit available in India?

Yes, term insurance offers tax benefits in India. The premium paid for a term insurance policy qualifies for a tax deduction under Section 80C of the Income Tax Act, up to ₹1.5 lakh per year. In addition, the death benefit received by the nominee is generally tax-free under Section 10(10D), provided the policy meets the prescribed conditions. This makes term insurance not only a strong financial protection tool but also a tax-efficient option for salaried individuals.

Is term insurance under 80C?

Yes, term insurance premiums are eligible for a tax deduction under Section 80C of the Income Tax Act, 1961. The premium you pay for a term insurance policy can be claimed as a deduction up to ₹1.5 lakh per year within the overall 80C limit. This benefit is available for policies taken for yourself, your spouse, or your children. However, the premium should generally not exceed 10% of the sum assured to qualify for the full tax benefit under Section 80C.

Is it worth buying term insurance?

Yes, term insurance is worth buying if you have financial dependents. It provides a large life cover at a low premium, ensuring your family’s financial security if something happens to you.