Table of Contents

ToggleFinancial Jungle: Are You Prepared to Get Out of It?

Personal finance often feels like a wild jungle — full of hidden traps like EMIs, credit card debt, and confusing “investment” products. In India, families are already carrying heavy loads: nearly one-third of take-home pay goes straight to EMIs before essentials like rent or groceries. When debt eats up more than 40% of income, experts warn it’s a serious red flag.

The deeper problem? Most people don’t know how to manage money wisely, save consistently, or invest safely. On top of that, mis-selling of insurance and mutual funds makes the jungle even more dangerous — with teachers, families, and even students falling prey to policies or schemes that don’t serve their real needs.

Survival in this financial jungle isn’t about luck. It’s about knowledge, planning, and the right financial tools. This guide is your map and compass to cross through the jungle safely, escape the monsters of debt and mis-selling, and build a secure path to wealth.

Monster Map (What We’ll Beat Today)

EMI Traps — when loans outgrow your income

Credit Card Debt — the silent monster in your wallet

Wrong Mutual Funds — chasing “hot” schemes

Wrong Insurance — paying more, getting less

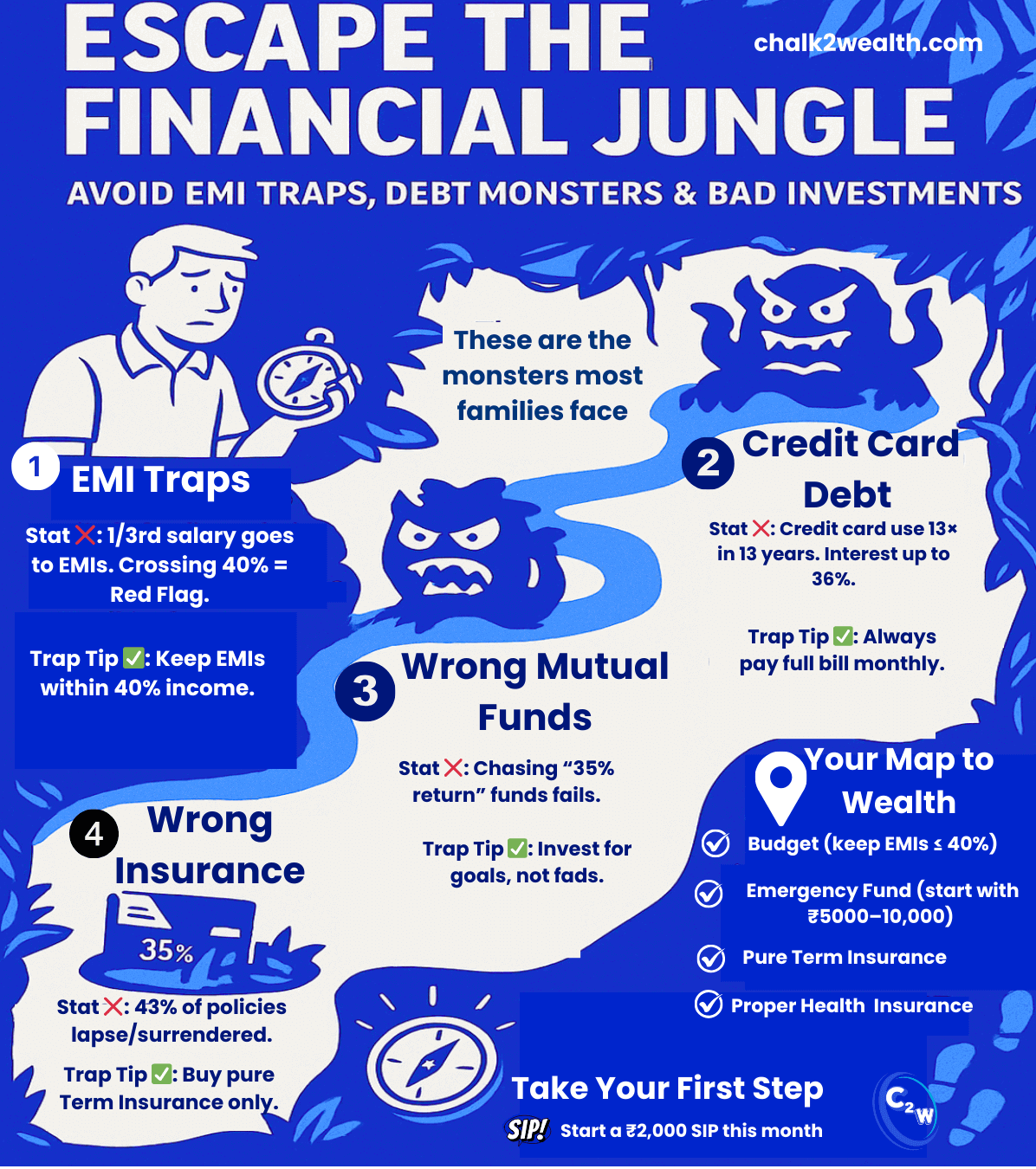

Monster 1 – EMI Traps in the Financial Jungle: When Loans Outgrow You

Easy monthly installments (EMIs) feel convenient — “buy now, pay later” for phones, fees, or gadgets — but they can quietly swallow your income. Indians now spend about 33% of salary on EMIs, and experts warn that crossing 40% is a red flag. Even education loans, like a mother paying ₹1.8 lakh per year fees via EMI, show how debt fuels stress instead of security.

How to Stay Safe:

- Budget for Debt: Keep total EMIs below 30–40% of income. Track using apps like Jupiter Money or FinArt.

- Build an Emergency Fund: Even ₹5k–10k helps avoid new borrowing.

- Clear High-Interest First: Pay off costly loans (credit card, BNPL) early.

- Skip Unnecessary EMIs: Save before you buy; SIPs can fund education without loans.

- Consolidate Smartly: Refinance or merge loans at lower interest, but read terms carefully.

By keeping EMIs in check, you avoid the debt trap and free money for savings and long-term goals. Instead of piling EMIs, see how a SIP can grow wealth here.

EMI Traps: Keep EMIs ≤40% of take-home; prepay the costliest EMI first.

2. Credit Card Debt in the Financial Jungle: The Silent Monster in Your Wallet

Credit cards are convenient but dangerous. In India, spending has surged 13× in 13 years (₹1.2 lakh crore → ₹15.6 lakh crore), and active users have grown from 2 crore to 10.8 crore. This easy credit often turns into crushing debt — with 24–36% annual interest, late fees, and the “minimum due” trap that makes small purchases spiral out of control. Many families end up rolling balances month after month, paying more in interest than for the things they bought.

What to Do:

- Pay in Full: Always clear the full statement; if not possible, pay well above the minimum.

- Track Spending: Use apps like Jupiter or Money Manager to categorize and cut wasteful expenses.

- Limit Cards: Reduce credit limits, freeze cards, or remove saved details to avoid impulse swipes.

- Avoid Cash Advances: These carry the highest fees; use only in emergencies.

- Negotiate Interest: With good history, ask banks for lower rates or EMI conversion of dues.

Managing card use with discipline frees your budget, improves savings, and safeguards your credit score. Check reports (CIBIL, Experian) regularly to spot rising debt early.

3. Mutual Funds in the Financial Jungle: Invest with Clarity, Not Fear

Mutual funds can be a powerful way to build wealth — but mistakes are common, especially among busy parents and new investors. One of the biggest errors is chasing hot funds: switching into a scheme just because it delivered 30% last year. Remember, past performance is no guarantee of future gains. Sectoral or tech funds that shine in a bull run can collapse just as quickly, turning winners into losers.

Before investing blindly, get the basics of mutual funds right here

Instead of running after “star” schemes, focus on your own goals. Are you saving for a house in 5 years, your child’s college in 10, or retirement in 30? The right mutual fund depends on your time horizon and risk tolerance: equity funds for long-term goals, and balanced/debt funds for shorter ones. Don’t fall for money myths about mutual funds — know the truth

What to Do:

Set Clear Goals: Define why and when you need the money. Goals determine how much risk you should take.

Use SIPs Wisely: Systematic Investment Plans let you invest monthly, buying more units when markets dip. Stay disciplined and avoid panic selling.

Diversify Smartly: Stick to 3–5 funds across categories (large-cap, mid/small-cap, debt). Too many funds dilute returns and create confusion.

Prefer Low-Cost Funds: Index funds or ETFs track the market with minimal fees, cutting out “manager risk.”

Review Annually: Check if your funds still fit your goals. Exit only if they consistently underperform or if your needs change.

In short, avoid fads and commissions. Don’t pour money into flashy schemes without understanding them. Skip the “hot” funds and instead build a simple, diversified, goal-based portfolio — investing directly, not through agents — so your money works harder for you.

4. Insurance in the Financial Jungle: Cover Risks, Don’t Chase Returns

Insurance is meant to provide protection, not serve as a savings scheme. Yet millions of Indians still buy endowment, money-back, or ULIP policies, often pushed by agents under the lure of tax benefits or guaranteed returns. The outcome is almost always the same — high premiums, low coverage, and regret. It’s no surprise that 43% of life insurance payouts in India are for lapsed or surrendered policies, proving how unsuitable these products are for most families.

What to Do:

- Buy Pure Term Insurance: Aim for cover worth 10–12× your annual income. A ₹50 lakh–₹1 crore term plan usually costs just a few thousand rupees a year and provides real protection.

- Avoid ULIPs and Endowment Plans: These products combine poor returns with inadequate cover. Use mutual funds or FDs for wealth-building — keep insurance separate.

- Compare Before You Buy: Check policies on IRDAI’s Bima Bharosa portal or through trusted aggregators. Always verify claim settlement ratios.

- Maintain Liquidity: Don’t lock all your money in premiums. If you already have unsuitable policies, consider exiting early. It’s better to take a small loss now than be trapped for years with poor returns.

In short: Treat insurance as a safety net, not an investment plan. The smartest strategy is term insurance for protection plus separate investments for growth.

Wrapping Up: Empower Your Financial Journey

The financial world may look like a jungle, but it’s one you can tame with the right mindset. Stay clear of EMI and credit card traps by living within your means and building a habit of saving. Invest in mutual funds with purpose, not panic. Buy insurance only for protection, not as a shortcut to wealth. And let technology be your ally in tracking every rupee. Start small with budgeting — 5 teacher-tested strategies can help you escape the jungle.

I write this not as a banker or a financial seller, but as a Headmaster in a government school in Himachal Pradesh, who has carved his own financial path slowly and steadily. Since 2009, I have been a student of personal finance — learning from Value Research, Moneylife, Outlook Money, Economic Times, Business Standard, and other financial newspapers and magazines, along with books that shaped my thinking on money and wealth. Every article, column, and book became a classroom where I picked up lessons that I then applied in real life.

Of course, the journey has not been perfect. Like many, I once paid unnecessary premiums, bought policies I didn’t need, and chased the wrong investments. But through continuous reading, reflection, and disciplined action, I discovered that knowledge and patience are the real weapons against the financial jungle.

That’s why I believe even teachers and middle-class families can turn financial stress into financial strength. Start small — set up a weekly budget envelope, create an emergency fund, or simply check your credit report. These tiny steps, when repeated, clear the path and turn the jungle into a garden you can manage with confidence.

At Chalk2Wealth, my mission is to share these hard-earned lessons with fellow educators, families, and students — so we can build a culture of financial literacy, honesty, and independence in India.

Because in the end, money should be your tool, not your trap.

“At Chalk2Wealth, we believe teachers, families, and students deserve money truth—not mis-selling. Subscribe, follow, and share—because when one teacher learns, an entire community benefits

Quick FAQ: Escaping the Financial Jungle

1. What do you mean by a “Financial Jungle”?

Personal finance in India often feels like a dense jungle—full of hidden traps like EMI overload, credit card debt, wrong mutual funds, and mis-sold insurance policies. Just like in a jungle, without a map or compass, people get lost. Here, the “map” is financial literacy, and the “compass” is smart money habits.

2. How much EMI is safe?

Keep EMIs within 40% of your income. Beyond this, you risk falling into a debt trap.

2. Why is credit card debt dangerous?

Because unpaid balances attract 40–45% annual interest. Always pay the full bill, not just the “minimum due.”

3. Are mutual funds risky?

Only if chosen blindly. Stick to goal-based SIPs in diversified or index funds and avoid chasing short-term returns.

4. What’s the best insurance for families?

Always choose pure term insurance for protection. Avoid endowment/money-back plans that give poor cover and high costs.

About the Author

Jagan Charak is the Headmaster of a government school in Himachal Pradesh and founder of Chalk2Wealth, a teacher-first financial literacy platform. He writes to help teachers and families understand money, avoid common traps like EMIs, credit card debt, and mis-sold insurance, and build long-term financial security.

This content is written for educational and informational purposes only. It is not financial advice. Please consult a qualified financial advisor before making investment decisions.

Exactly. Nice article.

🙏 Glad you found it useful. The financial jungle is real — EMIs, wrong policies, and debt traps silently eat away teachers’ and families’ savings. Together, through awareness and simple steps, we can escape it and build financial security.