Table of Contents

TogglePPF vs SIP in 2026: Which Investment Will Secure Your Future as a Teacher or Salaried Professional?

During a staffroom tea break, Mr. Sharma, a senior teacher, made a simple but worrying observation: “My salary increases every year, but prices seem to rise faster.” That one line captures the real meaning of financial security for teachers and salaried professionals—protecting today’s income from tomorrow’s higher costs of living.

This is where the decision between PPF vs SIP becomes crucial.

The Public Provident Fund (PPF) offers government-backed safety, tax benefits, and predictable returns. A SIP (Systematic Investment Plan) in mutual funds, on the other hand, is market-linked and designed to beat inflation over the long term. Yet many investors remain unsure. How safe is your money? How easily can you access it when needed? (explained in PPF Rules for Withdrawal (2026): How & When You Can Withdraw Your Money Safely). And is PPF alone enough for retirement, or should it be combined with growth-oriented options?

see PPF vs NPS: Which Is Better for Long-Term Retirement Savings for Teachers?

In this PPF vs SIP guide, we break down safety, returns, risk, and real-life suitability—so you can invest with clarity, confidence, and peace of mind.

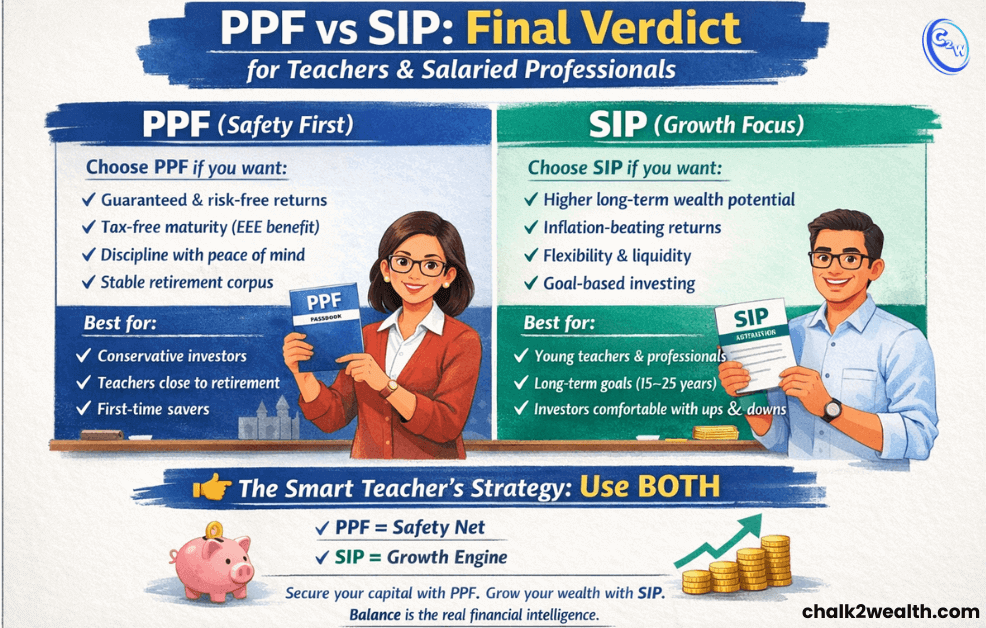

PPF for Stable Retirement Savings (Low-Risk Option in PPF vs SIP)

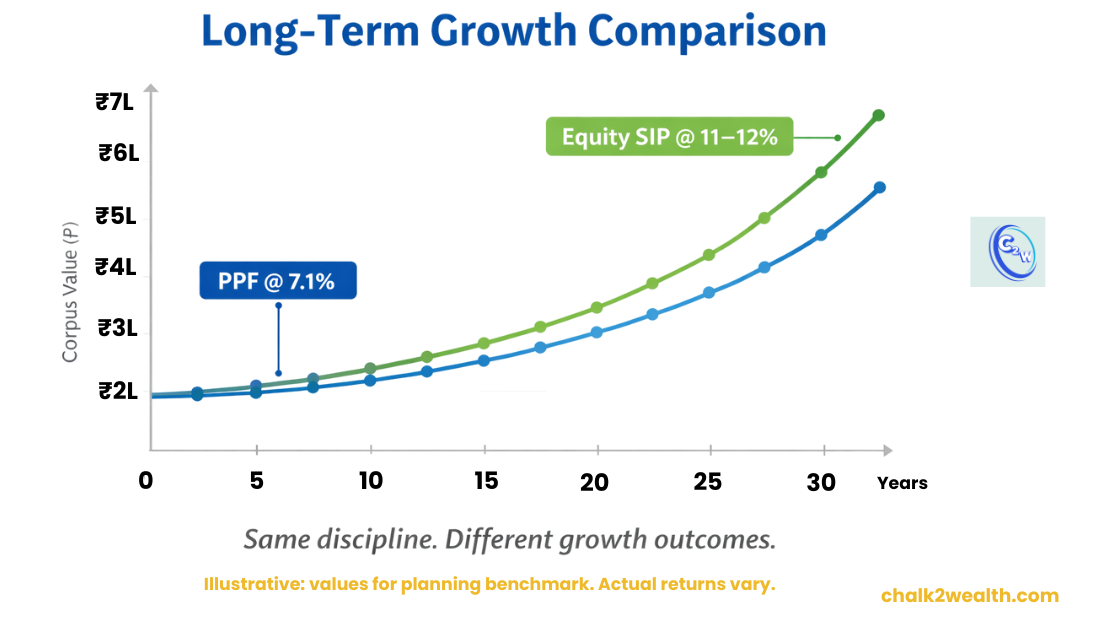

The Public Provident Fund (PPF) is a long-term, government-backed savings scheme best suited for teachers and salaried professionals seeking stability in retirement planning. You can invest between ₹500 and ₹1,50,000 per year, either as a lump sum or in instalments. PPF interest is calculated monthly on the balance before the 5th and credited annually. For 2026, the interest rate stands at 7.1% per annum, offering predictable, non-market-linked returns.

PPF is considered risk-free because returns are backed by the central government, not stock market performance. Its biggest strengths are capital safety and tax efficiency, with contributions eligible under Section 80C and the maturity amount remaining fully tax-free (EEE status).

The trade-off is liquidity. With a 15-year lock-in and limited withdrawal flexibility under PPF withdrawal rules, PPF works best as a core retirement-saving tool, not for short-term goals—an important point when evaluating PPF vs SIP.

SIP for Market-Linked Growth (Inflation-Beating Option in PPF vs SIP)

A Systematic Investment Plan (SIP) is a disciplined way of investing a fixed amount at regular intervals into a mutual fund—equity, debt, or hybrid. SIP instalments can start from ₹500 per month, making it suitable for monthly salary-based investing.

- Risk, Returns, and Investor Protection: SIPs are market-linked, which means returns fluctuate with market movements. AMFI clearly cautions that rupee-cost averaging does not guarantee profits or protect against losses during market declines. To help investors understand risk, SEBI mandates that every mutual fund scheme display a Riskometer, ranging from low to very high. It is important to note that SIP calculators are scenario-based tools. Even SEBI’s official SIP calculator requires you to enter an assumed rate of return to estimate a possible future value—these figures are projections, not promises.

- Expected Return Ranges (Planning Benchmarks for 2026): For investor-education illustrations, AMFI reports long-term averages based on historical rolling data:

Nifty 50 (equity): ~12.9% (10-year rolling average)

10-year government securities (debt): ~7.2%

Conservative hybrid (25% equity / 75% debt): ~8.6%

It is important to understand that SIP returns are market-linked and variable. SIP calculators—including SEBI’s official calculator—require users to assume a rate of return. These projections are illustrative, not promises.

To prevent unrealistic expectations, AMFI mandates that SIP and goal calculators:

Use return assumptions typically capped between 2% and 13%

Clearly disclose that past performance may or may not be sustained

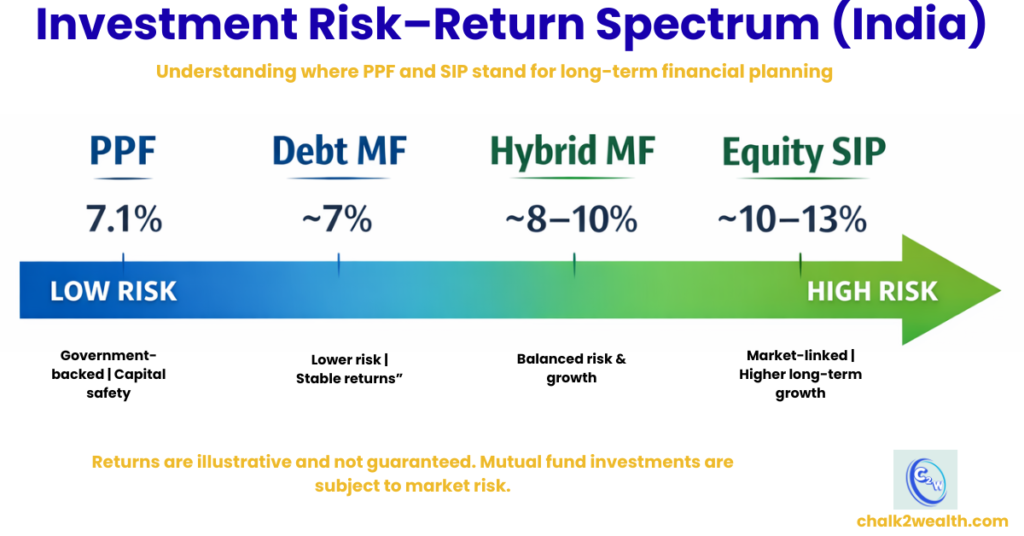

Illustrative Risk–Return Spectrum:

Lower risk/return → PPF (7.1%) | Debt MF (~7%) | Conservative Hybrid (~8–10%) | Equity MF (~10–13%) → Higher risk/returnThis spectrum helps position SIPs clearly on the growth side of the PPF vs SIP comparison.

PPF vs SIP: Key Differences at a Glance

| Attribute | PPF | SIP (Mutual Funds) |

|---|---|---|

| Risk | Sovereign-backed, non-market-linked; very high capital safety, but exposed to inflation and interest-rate risk | Market-linked; risk varies by scheme (Riskometer: low to very high) |

| Returns | 7.1% p.a. (Jan–Mar 2026 quarter) | Variable; planning ranges often use ~6–8% (debt), ~8–10% (hybrid), ~10–13% (equity); not guaranteed |

| Taxation | Section 80C benefit (within ₹1.5 lakh); EEE status (interest and withdrawals tax-free as explained in Is PPF Withdrawal Taxable from 2026? What Every Teacher Must Know) | Capital gains taxation applies; equity STCG 20%, equity LTCG 12.5% above ₹1.25 lakh (conditions apply); debt rules differ |

| Liquidity | Full withdrawal after 15 years; partial withdrawals allowed later but capped | Generally redeemable on working days; exit loads or lock-ins may apply depending on scheme |

| Minimum investment | Minimum ₹500 per year; maximum ₹1.5 lakh per year | SIPs often start from ₹500 per month (scheme-specific), and in some schemes even as low as ₹100. |

| Ideal time horizon | 15+ years | 7–10+ years for equity SIPs; shorter horizons possible for debt funds based on goals |

Quick Verdict: PPF vs SIP (2026)

- Choose PPF if capital safety, tax-free returns, and disciplined long-term saving matter more to you than high growth.

- Choose SIP (Mutual Funds) if you have a long time horizon (10+ years), can handle market ups and downs, and want to beat inflation.

- PPF alone is usually not enough to build inflation-proof retirement wealth.

- A combination of PPF + SIP works best for most teachers and salaried professionals.

Which Is Better for You: PPF or SIP?

If you are a teacher with a stable income and a clear retirement timeline, PPF works well as a core holding. Its 15-year tenure, EEE tax benefits, and freedom from market volatility make it ideal for disciplined, long-term retirement savings—though with limited liquidity.

If you are earlier in your career or have 10+ years before a major financial goal and can handle short-term ups and downs, an equity mutual fund SIP is usually the stronger option for wealth creation. The key is choosing schemes with a Riskometer level you are comfortable with and staying invested through market cycles.

For most educators, a balanced approach works best: use PPF as the stable, tax-efficient foundation and add an equity SIP for growth. Align this mix with your risk tolerance, emergency fund, and time horizon—and consider consulting a SEBI-registered investment adviser or a certified financial planner before making long-term commitments.

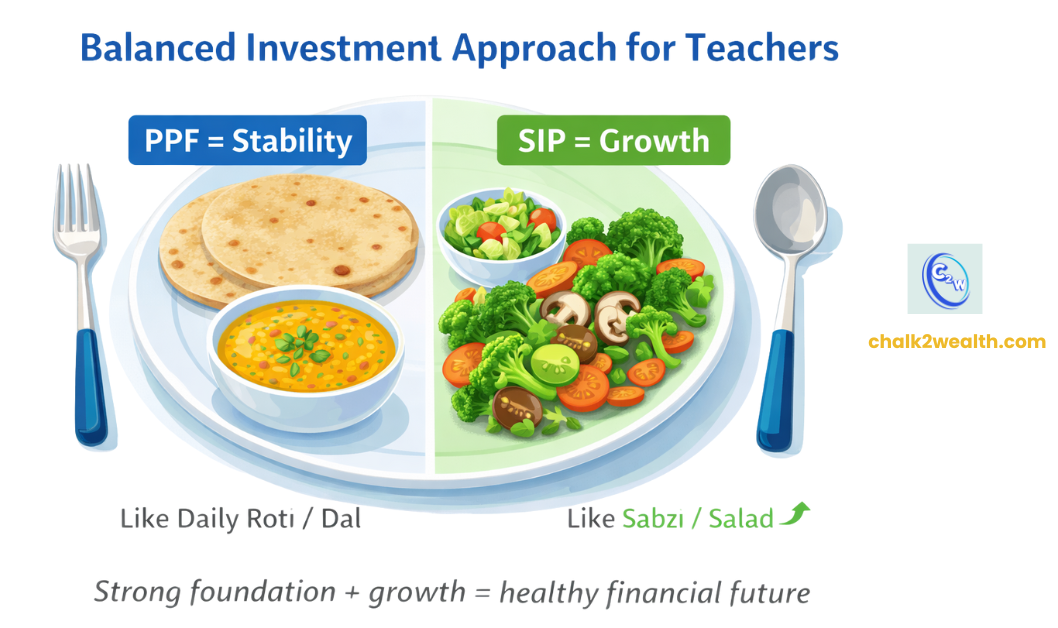

A Simple, Real-Life Illustration: PPF + SIP for Teachers

Think of your investments the way you think about food. For example, consider a 40-year-old school teacher with a stable salary and around 20 years left for retirement. In this case, PPF can act like the daily roti or dal—it provides basic nourishment in the form of safety, tax-free returns, and discipline. Alongside this, a monthly equity SIP of around ₹5,000 can be seen as sabzi or salad—slightly variable in taste but essential for long-term strength and growth. Relying only on PPF may keep savings safe, but it may struggle to beat inflation over long periods. On the other hand, relying only on market-linked SIPs can feel uncomfortable during market ups and downs. A balanced combination of PPF and SIP works much like a balanced meal—it keeps your financial foundation strong while gradually building long-term wealth.

This example is only for understanding purposes and is not a recommendation. Actual investment choices should depend on individual age, risk tolerance, and financial goals.

Disclaimer: This content is for informational purposes only and is not investment advice. Mutual fund investments are market-linked and subject to risk. Readers should verify current rules and consult a SEBI-registered investment adviser or financial planner before investing.