Table of Contents

ToggleWhy Term Insurance Claims Get Rejected and How Teachers Can Avoid It

A few days back, my brother-in-law — a college professor — read one of my Chalk2Wealth posts on insurance and said something that made me pause: “I think insurance is a scam. Even if you buy it, claims often get rejected when the family needs it most.” Aur sach kahun, yeh soch teachers aur middle-class families mein kaafi aam hai.

Many people believe that even after paying premiums for years, term insurance claims might still get rejected when the family files one. And unfortunately, that fear isn’t completely baseless. Some term insurance claims do get rejected — sometimes due to mis-selling, and sometimes because of small mistakes made while buying the policy.

At Chalk2Wealth, I’ve already explained the basics of protection plans in Term Life Insurance: Benefits, Myths & Is It Worth It in 2026 for Teachers? and compared policies in Term Insurance vs Endowment Plan: Which Saves More Money for Teachers in 2026?. These guides show why financial experts often recommend pure term insurance for maximum protection at the lowest cost.

But even after choosing the right policy, one big fear still remains: what if the claim gets rejected when your family needs it the most?

According to the Insurance Regulatory and Development Authority of India (IRDAI), 98.45% of individual life insurance death claims were settled in 2022–23. While that sounds reassuring, it also means a small percentage of claims were not paid — and for those families, the financial shock can be devastating. So why do term insurance claims get rejected, and how can teachers make sure their policy actually pays out when their family needs it the most? In this guide, we’ll break down the most common reasons term insurance claims get rejected in India — and the practical steps teachers can take to avoid those mistakes.

Term Insurance Claims: The Promise of Protection vs The Risk of Rejection

Term insurance is often chosen for its affordable high coverage — a ₹1 crore policy has become common among salaried professionals, including teachers. The promise is simple: if the insured person dies during the term, the insurer pays the sum assured to the nominee (usually a family member). On paper, it looks straightforward. But in practice, every policy carries conditions, and that’s where problems can arise.

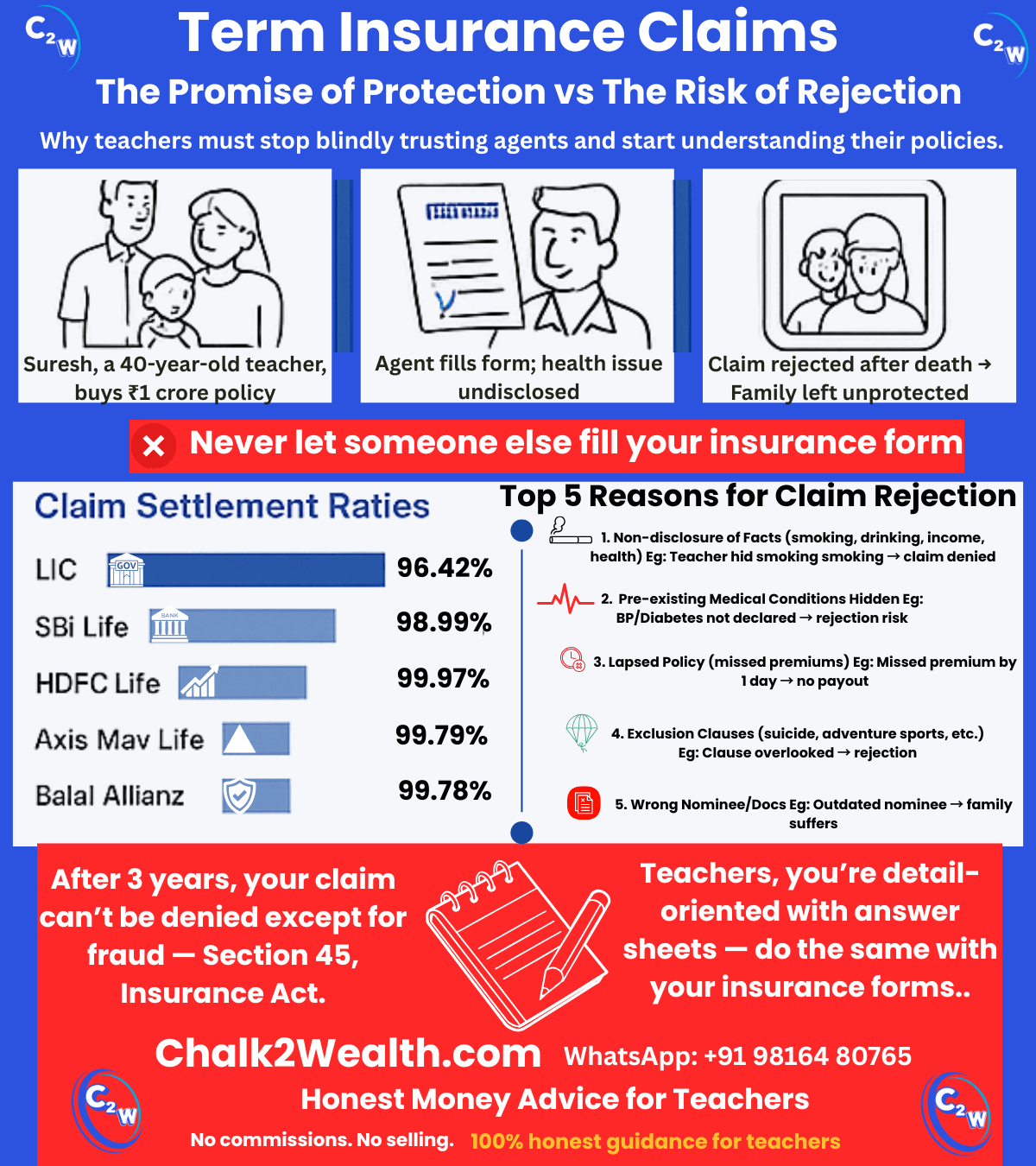

Take the case of Suresh, a 40-year-old school teacher from New Delhi. He purchased a ₹1 crore term plan to safeguard his wife and children. Trusting his insurance agent, he let the agent fill out the proposal form. Tragically, a few years later, Suresh passed away due to a health condition. When his wife filed the claim, it was rejected because the form had incomplete health details — a pre-existing illness hadn’t been disclosed. Despite his good intentions, the family was left unprotected (reported by Moneycontrol).

In fact, during one of our staffroom conversations, a colleague once admitted that he too had “just signed where the agent told me to.” Teachers are meticulous with exam answer sheets, but when it comes to insurance forms, even we sometimes rush — and that’s where trouble begins.

Such stories are not rare. They highlight how vital it is to get things right when buying a policy and throughout its term. Insurers do pay genuine term insurance claims, but they also invoke the fine print if there are gaps in disclosure or paperwork. Experts note that the risk of claim rejection rises sharply when incorrect, incomplete, or hidden information is present in the original application.

Quick Data Check

Claim Settlement Ratios of Life Insurers in 2025 (15,000+ Policies & LIC) -According to IRDAI’s latest Handbook on Indian Insurance Statistics (released in 2025, covering FY 2023–24 data)

| Insurance Company | Total Policies (2023–24) | Policies Paid Within 30 Days | % of Claims Paid Within 30 Days |

|---|---|---|---|

| LIC | 8,29,318 | 7,99,612 | 96.42% |

| SBI Life | 37,724 | 37,344 | 98.99% |

| Axis Max Life | 19,569 | 19,529 | 99.79% |

| HDFC Life | 19,338 | 19,333 | 99.97% |

| Bajaj Allianz | 14,695 | 14,662 | 99.78% |

Source: Handbook on Indian Insurance Statistics 2023–24, IRDAI; Economic Times

(All data pertains to 2023–24)

For teachers and middle-class families, the data tells two stories. On one hand, LIC dominates in sheer volume — handling over 8.29 lakh policies in 2023–24 — but its claim settlement ratio is 96.42%, lower than the private sector average. On the other hand, private insurers like HDFC Life (99.97%), Axis Max Life (99.79%), and Bajaj Allianz (99.78%) settle fewer policies overall, but boast near-perfect ratios. SBI Life also stands strong at 98.99% with significant volumes.

The takeaway for teachers? Don’t just go with the “most popular” option in your colony or staffroom. Look at both — reach and reliability — before choosing your plan.

Top Reasons Term Insurance Claims Get Rejected in India

Understanding why claims are denied can help you steer clear of those mistakes. Based on insurer reports and IRDAI insights, here are the five most common reasons for term insurance claim rejections:

1. Non-disclosure or False Information

When buying a term plan, the proposal form asks about age, income, occupation, lifestyle habits (smoking, drinking), health conditions, and existing policies. If any of this information is misrepresented — whether intentionally or by mistake — the claim can be denied later.

Example: Hiding smoking or alcohol use to get a lower premium is risky. If medical records show otherwise, insurers may reject the claim for misrepresentation. In Suresh’s case above, an undisclosed health issue became the reason for rejection.

2. Concealing Pre-existing Medical Conditions

Health history is a critical part of underwriting. Many applicants omit illnesses like diabetes, hypertension, or past surgeries fearing higher premiums. But this often backfires. If death occurs due to a long-standing condition that wasn’t declared, the insurer can repudiate the claim as “material non-disclosure.”

Bottom line: Always disclose medical history truthfully. Non-disclosure of health conditions remains one of the leading causes of claim rejection.

3. Policy Lapse Due to Non-Payment of Premiums

This is a surprisingly common reason. If premiums are not paid within the due date or grace period, the policy lapses. Any claim after that will not be honored — even if premiums were paid diligently in earlier years.

Example: A teacher misses his annual premium due in June, and the policy lapses in July. If he passes away in August, the claim will be denied. Even a one-day lapse can nullify the benefit.

4. Claims Falling Under Exclusion Clauses

All term policies have exclusions. The most common is suicide within the first policy year. Others may include death due to hazardous activities (racing, paragliding, scuba diving), illegal acts, or substance abuse.

While many modern term policies have reduced exclusions, families often face painful surprises when they assume “all deaths are covered.” Reading the exclusion list carefully is essential.

5. Nominee & Documentation Issues

Sometimes rejection happens not due to fraud, but due to paperwork gaps. If nominee details are outdated (for example, a parent was named but has since passed away) or if legal heirs are disputed, the claim may be delayed or denied until clarity is established.

Another factor is incomplete or late submission of documents like the death certificate, medical records, or ID proofs. Excessive delays in claim intimation can also trigger heavier scrutiny or rejection.

Key Insight

IRDAI data shows most insurers settle 98–99% of term insurance claims, but the small percentage of rejections usually comes down to these five reasons. By avoiding these pitfalls, you can ensure your family’s claim is honored without hurdles.

Sources: IRDAI Annual Report 2022–23; Moneycontrol; Economic Times

How to Avoid Term Insurance Claim Rejection

Follow this checklist to keep your term insurance claims rejection-proof.

- Fill the form yourself

Don’t let agents do it. Double-check all personal, health, lifestyle, and nominee details. Accuracy here prevents future disputes. - Disclose everything honestly

Mention all medical history, habits (smoking, drinking), and existing policies. Non-disclosure is the #1 reason claims get rejected. - Pay premiums on time

A lapsed policy = no coverage. Use auto-debit to avoid missing deadlines. Even a one-day lapse can void a claim. - Read the fine print

Know your policy’s exclusions (suicide clause, risky hobbies, etc.). Awareness now avoids painful surprises later. - Keep nominee details updated

Update nominee info if your life situation changes. Share policy details with your family so they know how to file a claim. - File claims promptly and correctly

Inform the insurer quickly, submit required documents (death certificate, ID, hospital records), and respond to queries without delay

Term insurance gives peace of mind — your family’s future is secure even if you’re not around. But that promise holds only if you do your part: be honest on the form, pay premiums on time, know the exclusions, and keep nominee details updated.

Remember, under Section 45 of the Insurance Act, once a policy crosses 3 years, insurers cannot reject claims except for fraud. So if you’ve been truthful, your family’s claim is almost certain to be paid.

Bottom line: treat your policy like a key financial document. Maintain it well, keep your family informed, and you’ll ensure that when it matters most, your term insurance truly delivers.

Teachers, make your term insurance claims 100% claim-ready today. review your policy form, update nominee details, and mark your premium dates. A 10-minute check now can save your family months of financial stress later.

FAQs on Term Insurance Claims

What is the term insurance claim settlement ratio and why is it important?

The term insurance claim settlement ratio shows the percentage of insurance claims an insurer successfully pays compared to the total claims received in a year. For example, if an insurance company has a claim settlement ratio of 98%, it means that out of 100 claims filed, about 98 claims were settled and paid to the nominees. A higher term insurance claim settlement ratio generally indicates better reliability of the insurer, but policyholders should also focus on honest disclosure of health, income, and lifestyle details while buying the policy to avoid claim rejection.

What is the term insurance claim ratio?

The term insurance claim ratio, also known as the claim settlement ratio, indicates the percentage of claims that an insurance company successfully settles compared to the total number of claims received in a year. For example, if an insurer has a term insurance claim ratio of 98%, it means that out of 100 claims filed, about 98 claims were paid to the nominees. A higher term insurance claim ratio generally indicates better reliability of the insurer, but policyholders should still disclose all health, lifestyle, and income details honestly to avoid claim rejection.

What are the common term insurance claim rejection reasons?

The most common term insurance claim rejection reasons include non-disclosure of health conditions, hiding habits like smoking or drinking, incorrect income details, lapsed policies due to missed premium payments, and ignoring exclusion clauses in the policy. Claims may also be rejected if nominee details or required documents are incorrect. To avoid claim rejection, policyholders should always fill the proposal form themselves and disclose all medical and lifestyle information honestly while buying term insurance.

Is term insurance and life insurance the same?

Term insurance is a type of life insurance, but they are not exactly the same. Life insurance is a broad category that includes different policies such as term insurance, endowment plans, and whole life insurance. Term insurance is the simplest form of life insurance that provides pure financial protection for a specific period (term) without any savings or investment component. Because of this, term insurance usually offers a much higher life cover at a lower premium compared to other life insurance plans.

Is there any tax on term insurance claim in India?

No, the amount received from a term insurance claim is generally tax-free in India. Under Section 10(10D) of the Income Tax Act, the death benefit paid to the nominee after the policyholder’s death is fully exempt from income tax. This means the family receives the entire claim amount without any tax deduction, making term insurance a reliable financial protection tool for dependents.

How to claim term insurance in India?

To claim term insurance, the nominee must inform the insurance company about the policyholder’s death as soon as possible. The nominee then needs to submit the claim form along with required documents such as the death certificate, policy document, identity proof, and bank details. Once the insurer verifies the documents and details, the claim amount is paid to the nominee according to the policy terms.

What is the term insurance claim process in India?

The term insurance claim process begins when the nominee informs the insurance company about the policyholder’s death. The nominee must then submit the claim form along with necessary documents such as the death certificate, policy document, identity proof, and bank details. After verifying the documents and policy details, the insurer reviews the claim and, if everything is correct, releases the claim amount to the nominee as per the policy terms.

About the Author

Jagan Charak is the Headmaster of a government school in Himachal Pradesh and founder of Chalk2Wealth, a teacher-first financial literacy platform. He writes to help teachers and families understand money, avoid common traps like EMIs, credit card debt, and mis-sold insurance, and build long-term financial security.

This content is written for educational and informational purposes only. It is not financial advice. Please consult a qualified financial advisor before making investment decisions.

Also Read on Chalk2Wealth

7 Costly Term Insurance Mistakes Teachers Still Make in 2025

Term Life Insurance for Teachers in India 2025: Honest Guide

Which of these five reasons for claim rejection surprised you the most? Do you think teachers are aware of these risks? let me know in comments or whatsapp 9816480765

Nice article.

Thank you, Surjeet ji! 🙏 I’m glad you found the article useful. Most people focus only on buying insurance but forget that small mistakes in disclosure or paperwork can cost families later. That’s why awareness is the first protection. Keep following Chalk2Wealth—we’ll keep bringing more teacher-friendly money insights.