Table of Contents

ToggleTerm Insurance vs ULIP (2026): Why Teachers Are Switching to Pure Protection

“Sir, ULIP mein insurance bhi hai aur investment bhi — double benefit.”

Many teachers in India have heard this line from an insurance agent at least once.

At first, the idea sounds logical. If a single product offers both life insurance protection and investment returns, why buy two different products?

But the reality is often more complicated.

ULIPs (Unit Linked Insurance Plans) combine insurance and market-linked investments in one policy. However, the sales pitch usually skips some important details — multiple charges, long lock-in periods, and returns that depend on market performance.

Term insurance works very differently. It focuses purely on financial protection for your family if something happens to you during the policy term.

If you want to understand why many financial experts recommend pure protection, read our detailed comparison on Term Insurance vs Endowment Plan where we explain how traditional insurance plans compare with term insurance.

You may also want to learn about the common mistakes people make while buying insurance in our guide on Why Term Insurance is Important: 7 Costly Mistakes.

For a conservative salaried professional like a teacher, protection and savings are both important — but they do not always need to come from the same product.

Term Insurance vs ULIP: Key Differences Explained

When comparing Term Insurance vs ULIP, many teachers assume both products serve the same purpose. In reality, they are designed for very different financial goals. Term insurance focuses purely on providing financial protection to your family, while ULIPs (Unit Linked Insurance Plans) combine life insurance with market-linked investment.

The table below explains the key differences between term insurance and ULIP in a simple way.

| Topic | Term Insurance | ULIP |

|---|---|---|

| Purpose | Family protection (life cover) | Life cover + market-linked investment |

| Risk level | Low (not linked to market performance) | Market risk is borne by the investor |

| Returns | No maturity return in a normal term plan | Depends on fund performance |

| Premium cost | Low premium for high coverage | Higher because of investment component |

| Charges | Simple premium structure | Multiple deductions and charges |

| Maturity benefit | Not payable in a normal term plan | Fund value paid on maturity |

| Transparency | Easier to understand | Requires careful reading of policy illustration |

| Best suited for | People seeking strong life cover | Long-term investors comfortable with market risk |

Returns Comparison

When comparing Term Insurance vs ULIP, the biggest confusion is about returns.

A standard term insurance plan has no maturity payout because it is designed purely for life protection. Some policies offer a Return of Premium (ROP) option, where premiums are refunded at maturity, but these plans usually cost significantly more than a pure term plan.

ULIP returns depend on market performance.

Your premium is divided into three parts:

• life cover

• policy charges

• investment in market-linked funds

Because of this structure, the final maturity value can rise or fall depending on market conditions.

As a long-term reference, data from the National Stock Exchange of India shows that the Nifty 50 Total Return Index delivered about 11.8% CAGR over 15 years (data as of December 2021). However, this should be viewed only as a historical indication, not a guaranteed outcome. The Securities and Exchange Board of India (SEBI) also clearly states that market-linked investments do not guarantee returns or capital protection, so projected numbers in illustrations should not be treated as certainty.

Key Takeaway: In the Term Insurance vs ULIP debate, returns are uncertain in ULIPs because they depend on markets and charges. Term insurance, on the other hand, focuses purely on providing high life cover at a lower cost, keeping protection separate from investment.

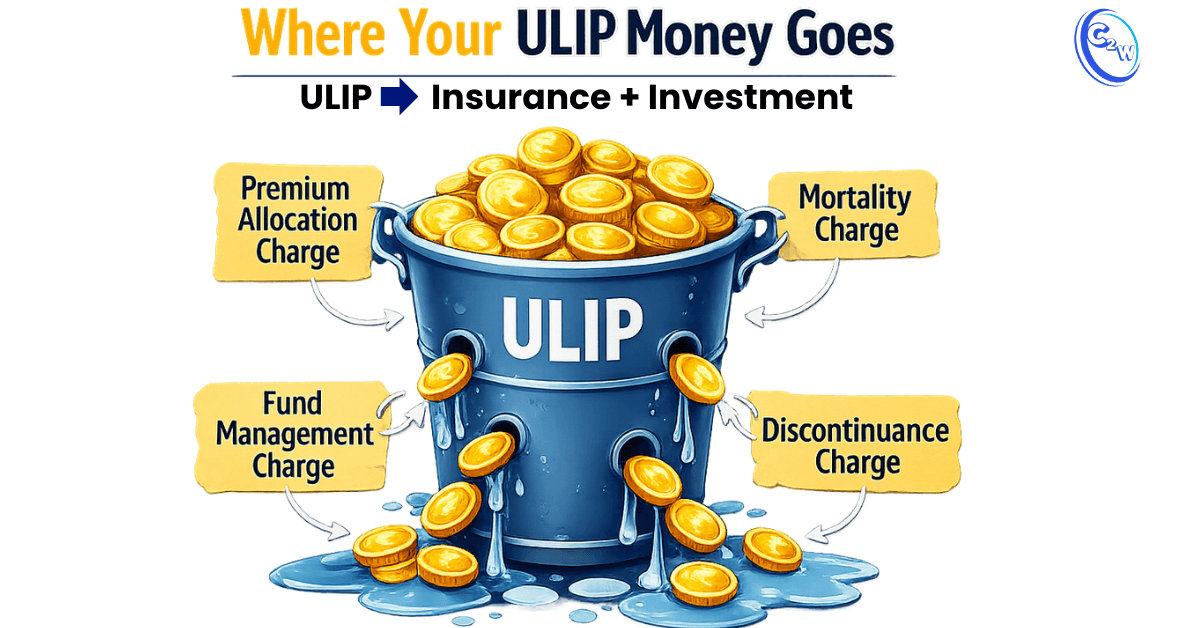

Cost & Hidden Charges

Cost is one of the biggest differences in the Term Insurance vs ULIP comparison.

For example, a typical illustration for a 30-year-old male seeking ₹1 crore cover shows a pure term plan costing around ₹9,135 per year (excluding GST).

In contrast, some ULIP brochures show annual premiums of about ₹80,000 for 10 years.

The reason for this gap is that ULIPs include multiple charges, such as:

- Premium allocation charge

- Fund management charge

- Mortality charge (cost of life cover)

- Discontinuance or surrender charges if the policy is exited early

The Insurance Regulatory and Development Authority of India (IRDAI) places limits on these charges. For example, premium allocation charges are capped at 12.5% of the annualised premium, and fund management charges are capped at 1.35% per year per fund.

If you want to see how term insurance compares with traditional insurance plans on cost and savings, you can also read our detailed guide on term insurance vs endowment plan for teachers.

Key Takeaway : In the Term Insurance vs ULIP debate, the major cost advantage of term insurance is clear. A practical rule many teachers follow is simple: buy term insurance for protection and invest separately for growth. This approach usually provides higher life cover at a lower cost while avoiding the charge structure of ULIPs.

Safety and Risk Level

In the Term Insurance vs ULIP comparison, the risk level is very different. Term insurance is safety-focused. The payout to your family is not linked to market performance. As long as the policy is active and the insured event occurs during the policy term, the nominee receives the sum assured. ULIPs are market-linked products. The investment portion of your premium is invested in equity or debt funds, so the final value depends on market performance.

Understanding how claims work is also important. Teachers should be aware of the common reasons term insurance claims get rejected and how simple steps like correct disclosure can help avoid problems later.

ULIPs are market-linked products. The investment portion of your premium is invested in equity or debt funds, so the final value depends on market performance.

Regulations also require ULIPs to clearly disclose that there is no liquidity during the first five years. This means full surrender or withdrawals are generally not allowed until the completion of the fifth policy year.

Why Teachers Are Switching to Pure Term Insurance

Illustrative example. Actual premiums vary by age, insurer and policy terms.

Several practical reasons explain why many teachers are moving toward pure term insurance instead of bundled products like ULIPs.

- Higher life cover at lower cost: A term plan can provide ₹1 crore cover at a fraction of the premium required in many ULIPs.

- Simpler financial planning: Insurance and investment are kept separate, making it easier to track both.

- Better transparency: Term plans are straightforward, while ULIPs involve multiple charges and fund choices.

- Flexibility in investments: Teachers can choose investments separately based on goals and risk tolerance.

For many conservative salaried professionals, this approach keeps financial protection simple and efficient.

Real-Life Suitability

- Teachers with fixed salary: Start with term insurance for family protection; keep investments separate for better discipline.

- Young salaried employees: Lock in a higher term cover early while premiums are low, then build investments gradually.

- Beginners: Avoid starting with ULIPs; early exits can hurt due to the 5-year lock-in and discontinuance rules.

- Long-term investors: Consider ULIPs only after adequate term cover is secured and only if you are willing to track charges and fund performance.

Pros and Cons: Term Insurance vs ULIP

| Factor | Term Insurance | ULIP |

|---|---|---|

| Life cover | Very high for low premium | Lower cover due to investment component |

| Investment | None | Market-linked investment |

| Charges | Simple premium | Multiple charges |

| Flexibility | High | Limited due to lock-in |

| Transparency | Easy to understand | Requires careful policy reading |

| Best for | Family protection | Long-term investors comfortable with market risk |

Term Insurance vs ULIP: Final Verdict for Teachers

For most Indian teachers and conservative salaried professionals, term insurance is usually the better option for life cover. It provides strong family protection at a much lower cost, without market risk or complicated charge deductions.

ULIPs may suit investors who already have adequate term insurance and want market-linked investment inside an insurance policy, while being comfortable with the five-year lock-in and ongoing charges.

Bottom Line

If the question is “Term Insurance vs ULIP: which is better for teachers?”

The practical approach is simple:

Buy term insurance for protection and invest separately for long-term wealth creation.

Term Insurance vs ULIP: FAQ

Which is better: term plan vs ULIP for teachers?

In most cases, term plan vs ULIP comparisons show that a term plan is better for pure life insurance protection. A term plan offers higher life cover at a much lower premium because it focuses only on insurance. A ULIP, on the other hand, combines insurance with market-linked investment. Part of the premium goes toward policy charges and investment funds, so the life cover for the same premium is usually lower compared to a term plan.

For many teachers and conservative salaried professionals, a common strategy is to buy a term plan for family protection and invest separately for long-term wealth creation.

What is the difference between ULIP and term insurance?

The main difference between ULIP and term insurance is their purpose. Term insurance is a pure life insurance product that provides financial protection to your family at a relatively low premium. It does not include any investment component.

A ULIP (Unit Linked Insurance Plan) combines life insurance with market-linked investment. Part of the premium pays for insurance coverage, while the remaining amount is invested in equity or debt funds. Because of this structure, ULIPs involve market risk and multiple charges, whereas term insurance focuses only on providing affordable life cover.

Term insurance vs ULIP: which is better?

In the term insurance vs ULIP which is better comparison, the answer depends on your financial goal. If your priority is pure life protection, a term insurance plan is usually better because it provides a much higher life cover at a lower premium. A ULIP (Unit Linked Insurance Plan) combines insurance with market-linked investment, where part of the premium is invested in funds and part goes toward charges and life cover. Because of these charges and market risk, the life cover for the same premium is usually lower than a term plan.

For many teachers and conservative salaried professionals, a practical approach is to buy term insurance for family protection and invest separately for long-term wealth creation.

After a very long time but a very informative topic sir

Thank you Rajan Sir. Glad you found the topic informative. I keep sharing such financial insights for teachers on my blog as well.