Table of Contents

ToggleTerm Insurance Tax Benefit Under Which Section? (80C & 10(10D) Guide 2026)

Last week in the staffroom, a colleague asked me a simple but uncomfortable question:

“Term insurance tax benefit comes under which section?”

What shocked me wasn’t the question—it was how many of us didn’t know the answer.

We pay premiums every year.

We believe we are “saving tax.”

But very few actually understand how much we save, under which section, and what our family really gets in return. In fact, most teachers are still confused not just about tax—but also about how much term insurance cover they actually need for their family.

Let’s make it crystal clear:

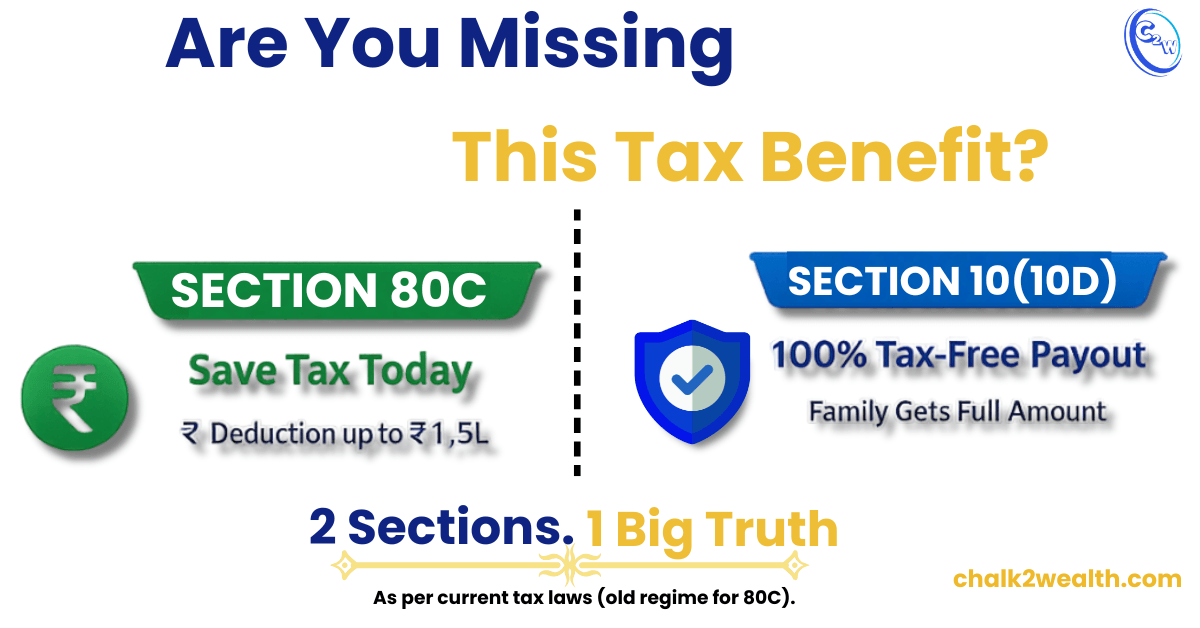

Term insurance tax benefit comes under Section 80C (for premium deduction) and Section 10(10D) (for tax-free payout).

That’s it. Two sections.

One reduces your tax today.

The other protects your family tomorrow—without any tax burden.

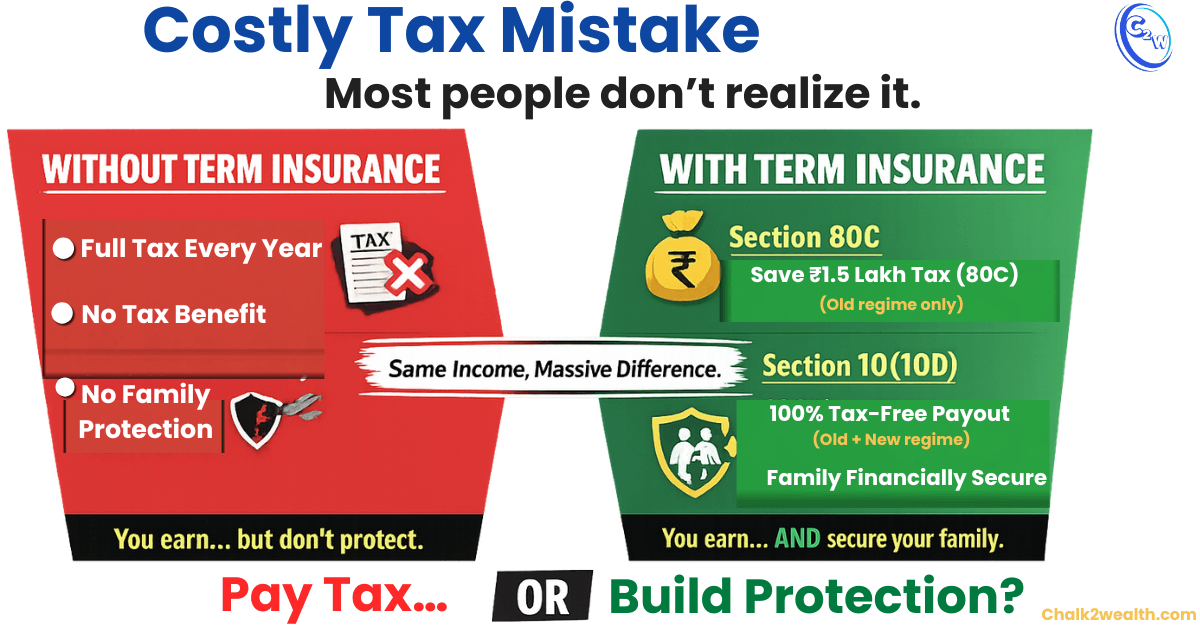

But here’s the uncomfortable truth most people ignore:

- Many people buy insurance only for tax saving…

- And completely miss its real purpose—financial protection.

In this guide, I’ll break down both sections in simple terms, show you how to claim these benefits correctly, and help you avoid the common mistakes that silently cost families lakhs.

Because tax saving is just a bonus.

Protection is the real reason you buy term insurance. (We’ll also briefly compare Term Insurance vs Endowment to give better context.)

Quick Answer: Term Insurance Tax Benefit

Section 80C → Deduction on premium (up to ₹1.5 lakh)

Section 10(10D) → Tax-free payout

80C → Only old regime

10(10D) → Applies in both regimes

What Does Term Insurance Tax Benefit Mean? (Sections 80C & 10(10D) Explained)

Term Insurance Tax Benefits (Quick Comparison)

| Feature | Section 80C | Section 10(10D) |

|---|---|---|

| Type of Benefit | Tax Deduction | Tax Exemption |

| When It Applies | While paying premium | When payout is received |

| Who Benefits | Policyholder | Nominee / Family |

| Maximum Limit | ₹1.5 lakh (within 80C limit) | No limit (generally tax-free) |

| Applicable Regime | Only Old Tax Regime | Both Old & New Regime |

| Purpose | Reduce taxable income | Ensure tax-free financial support |

| Condition | Premium ≤ 10% of sum assured | Standard conditions apply |

Note: Tax benefits are subject to current income tax laws. Section 80C applies only under the old regime, while Section 10(10D) exemption is generally available under both regimes, subject to conditions.

In simple terms, term insurance offers two powerful tax advantages under Indian tax laws—one while you pay, and one when your family receives the benefit.

1. Tax Deduction on Premium (Section 80C): The premium you pay for your term insurance policy is eligible for deduction under Section 80C (up to ₹1.5 lakh per year, within the overall limit).

This directly reduces your taxable income, helping you save tax every year.

Note: This benefit is available only under the old tax regime. If you choose the new tax regime, you cannot claim this deduction.

2. Tax-Free Payout (Section 10(10D)): The amount your nominee receives—whether as a death benefit or maturity (if applicable)—is completely tax-free under Section 10(10D), subject to standard conditions. This ensures your family gets the full financial support without any tax burden.This is one of the key reasons why many experts consider term insurance as one of the most efficient protection tools for families, especially when compared with other traditional plans like endowment policies.

Good news: This tax-free benefit under Section 10(10D) is part of the answer to “term insurance tax benefit under which section,” and it generally applies under both old and new tax regimes, as it is an exemption, not a deduction.

Section 80C: Term Insurance Tax Benefit Explained

When you ask “term insurance tax benefit comes under which section,” this is the first part of the answer. Under Section 80C, the premium you pay for term insurance is eligible for deduction up to ₹1.5 lakh per year (combined with other 80C investments).

Example: A teacher earning ₹40,000/month paying ₹12,000/year as premium can claim the full amount as a deduction—reducing taxable income.

Key Rules

- Who is covered: Self, spouse, or children

- 10% rule: Premium ≤ 10% of sum assured (for policies after 1 April 2012)

- Minimum period: Continue policy for at least 2 years, or deductions get reversed

- Shared limit: ₹1.5 lakh includes PPF, EPF, ELSS, etc.

Important Note This term insurance tax benefit under Section 80C is available only under the old tax regime. Your premium becomes a simple way to claim tax benefit under Section 80C and reduce taxable income—just like other safe options such as PPF and tax-saving investments commonly used by teachers.

Section 10(10D): Tax-Free Payout Explained

When asking “term insurance tax benefit under which section,” this is the second and most powerful part of the answer.

Under Section 10(10D), the amount your nominee receives from a life insurance policy is completely tax-free, making it one of the biggest advantages of term insurance—and one of the key reasons why financial experts strongly emphasize the importance of having adequate life cover.

What Is Tax-Free?

- Death benefit: The full amount received by your nominee is 100% tax-free, with no limit or condition on premium ratio

- Maturity proceeds (if applicable):Pure term insurance usually does not give any maturity amount. But if your plan has a return (like “return of premium”), that amount is tax-free only if the premium stays within allowed limits.

Key Conditions to Remember

- For policies issued on/after 1 April 2012, annual premium must not exceed 10% of sum assured

- For policies issued on/after 1 April 2023, the total annual premium should not exceed ₹5 lakh to keep maturity proceeds tax-free

- If these conditions are not met, maturity payout may become taxable

This part of the term insurance tax benefit under Section 10(10D) generally applies under both old and new tax regimes, as it is an exemption—not a deduction.

When Term Insurance Tax Benefit Is NOT Available

If you’re wondering “term insurance tax benefit under which section,” it’s equally important to know when these benefits do not apply.

- Premium Exceeds Limits: If the premium exceeds 10% of sum assured (for policies after April 2012):

- Section 80C deduction may be restricted

- Section 10(10D) exemption on maturity may not apply

2. Policy Lapses or Is Surrendered Early: If you stop premiums or surrender before 2 years:

- Earlier 80C deductions can be reversed

- Policy benefits are lost

3. Incorrect or False Information: If wrong details are provided and the claim is rejected:

- Your family may not receive the payout

- Tax benefits become meaningless

This is exactly why understanding common reasons why term insurance claims get rejected and how to avoid them becomes critical before buying a policy.

Bottom Line: Stay within limits, keep the policy active, and provide accurate details to enjoy full tax benefits

How to Claim ₹1.5 Lakh Deduction Under Section 80C

If you’re asking “term insurance tax benefit under which section,” you can claim it under Section 80C in two simple ways:

Through Employer:: Submit premium receipts + Form 12BB to HR. Your employer reflects it in Form 16, reducing taxable salary

While Filing ITR: Enter the premium under Section 80C and keep payment proof ready

Final Verdict

For teachers and salaried professionals, term insurance is both a protection tool and a tax saver. You can claim up to ₹1.5 lakh deduction under Section 80C, and the payout remains tax-free under Section 10(10D).

But remember—don’t buy term insurance just for tax saving.

Its real purpose is to secure your family’s future.

If you’re still unsure whether term insurance is actually worth it for you or just another tax-saving product, take a moment to understand the bigger picture before making a decision.

Tax benefit is a bonus. Protection is the purpose.

Disclaimer: This article on “term insurance tax benefit under which section” is for educational purposes only. Tax laws may change and vary by individual situation. Please consult a qualified tax advisor before making decisions.