Table of Contents

TogglePPF Interest Calculation (2026): Formula, Interest Date & PPF Calculator Explained

Last month in the staffroom, a colleague asked me a simple question. “Sir, I deposit money in my PPF account every month. But someone told me the date of deposit affects the interest. Is that true?”

Most teachers know that the PPF interest rate in 2026 is around 7.1%, but very few understand how that interest is actually calculated. Here is the rule most investors miss: PPF interest is calculated on the lowest balance between the 5th and the last day of each month.

That means one small mistake—depositing after the 5th—can quietly reduce your returns.

In fact, if you invest ₹1.5 lakh every year but deposit after the 5th each time, you could lose ₹40,000–₹60,000 over 15 years, simply because of timing.

This is not about investing more. It’s about investing at the right time.

In this guide, we will explain:

- The exact PPF interest calculation formula

- The 5th-day rule (with real examples)

- How to estimate returns using a PPF calculator

Also read: How to Check PPF Balance Online and PPF Withdrawal Rules.

PPF Interest Calculation (Quick Answer)

PPF interest is calculated monthly based on the lowest balance between the 5th and the last day of each month. The interest is then credited once a year on 31 March.

To earn full interest for a month, deposits should be made on or before the 5th.

PPF Interest Calculation: How PPF Interest Is Calculated

To understand how PPF interest is calculated, remember two simple rules used in the official PPF scheme. If you’re new to this scheme, it’s helpful to first understand what is Public Provident Fund (PPF) and how it works before going deeper into interest calculation.

According to the Public Provident Fund Scheme notified by the Government of India, interest is calculated on the lowest balance between the 5th and the last day of each month.

1. Lowest balance rule: The government calculates interest based on the lowest balance in your PPF account between the close of the 5th day and the last day of each month.

This amount becomes your interest-eligible balance for that month.

2. Monthly calculation, yearly credit: PPF interest is calculated every month, but it is credited to your account once at the end of the financial year (31 March). You can also check your PPF balance online to see how this interest is added to your account each year.

PPF Interest Calculation Formula

The basic PPF interest calculation formula is:

Monthly Interest = (Lowest balance × Interest rate) / 1200

Since the PPF interest rate is annual, the monthly interest is effectively the yearly amount divided by 12 months. Banks and post offices calculate interest for each month, add all monthly amounts together, and then credit the total interest at the end of the financial year. To understand whether this interest is actually helping your money grow in real terms, you can also read PPF interest vs inflation.

Important PPF Interest Calculation Date Rule

To maximise returns, follow one important rule: Deposit money in your PPF account on or before the 5th of the month. If the deposit is made after the 5th, that amount usually starts earning interest from the next month, which means you lose one month of potential interest.

Over long periods, this small delay can reduce your overall returns through compounding. If you want to understand how this affects real growth, you can also read PPF interest vs inflation.

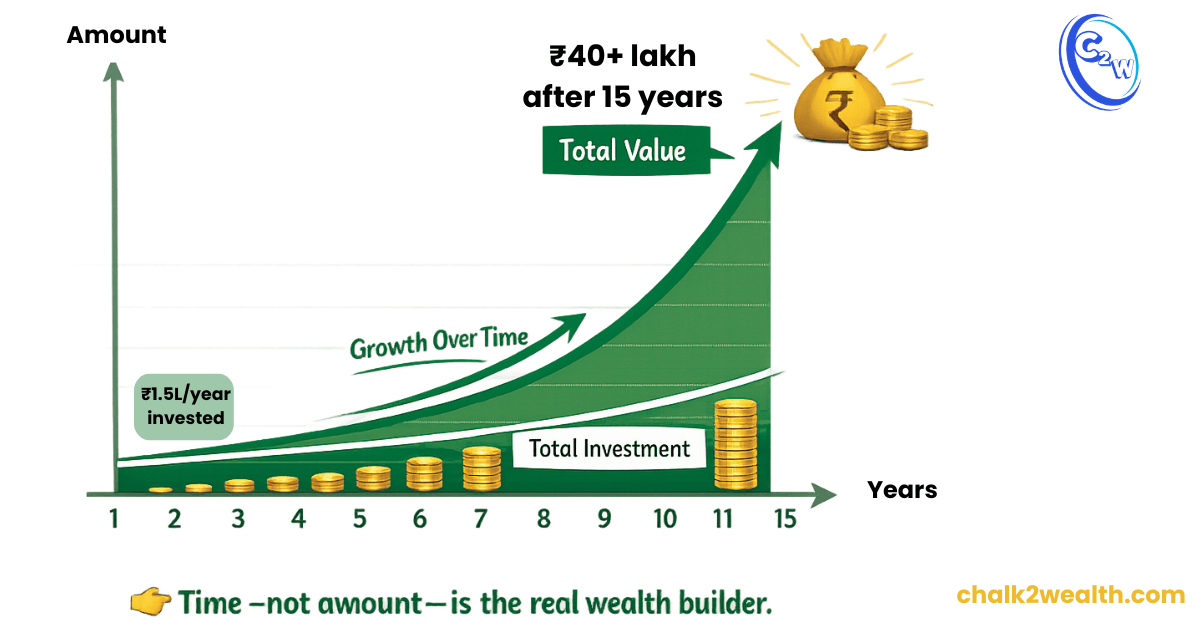

PPF Interest Calculation Example (Real Impact)

Let’s understand this with a realistic long-term example that most teachers can relate to.

Scenario:

- Investment: ₹1.5 lakh per year (maximum allowed)

- Interest rate: 7.1%

- Tenure: 15 years

Case 1: Deposit BEFORE 5th (Correct Strategy)

- Full amount is counted for that month’s interest

- No loss of interest window

Approx. result after 15 years:

| Item | Value |

|---|---|

| Total invested | ₹22.5 lakh |

| Interest earned | ~₹18.2 lakh |

| Final amount | ₹40–41 lakh |

Case 2: Deposit AFTER 5th (Common Mistake)

- One month interest is missed every year

- Compounding effect slightly reduces

Estimated impact over 15 years:

- Loss in interest: ₹40,000–₹60,000

- Final amount slightly lower than optimal scenario

What This Means: At first glance, missing one month of interest may seem small. But over time, this small delay compounds into a noticeable loss. In PPF, timing your deposit is often more important than increasing your investment amount.

Simple Rule to Remember

- Deposit on or before the 5th = full benefit

- Deposit after the 5th = delayed growth

When Does PPF Interest Get Credited?

Many investors ask, when PPF interest will be credited in their account. Although PPF interest is calculated every month, it is not credited monthly. The government credits the accumulated interest once a year on 31 March, at the end of the financial year. This means your account balance increases only once per year, but the interest calculation is happening internally every month based on the lowest balance between the 5th and the last day of each month. You can also check your PPF balance online to see how this yearly interest credit reflects in your account.

After the interest is credited on 31 March, the new balance becomes the base for the next year’s compounding. Because of this yearly credit system, PPF works best as a long-term compounding investment, especially when deposits are made regularly and before the 5th of the month. If you’re planning long-term, you should also understand PPF extension rules after 15 years.

PPF Interest Calculation Date Rule

The PPF interest calculation date rule is simple but very important.

Rule: Interest for a month is calculated on the lowest balance between the 5th and the last day of that month. Even a small delay can affect interest.

| Deposit Date | Interest for That Month |

|---|---|

| 4 April | Yes (counts for April) |

| 7 April | No (interest starts from May) |

Practical tip: If investing a yearly lump sum, try to deposit before 5 April so the money earns interest from April itself.

PPF Interest Rate Calculator

A PPF interest rate calculator helps you estimate your maturity value without doing manual calculations. Many investors use a PPF interest rate calculator available on bank websites or financial portals to estimate maturity values quickly.

You can find one on:

- bank websites

- finance portals

- government savings portals for official rate updates

Most calculators ask for:

- yearly or monthly investment

- interest rate (7.1% for 2026)

- tenure (15 years standard)

One important point: a calculator gives only an estimate. Your actual maturity amount can vary because of the 5th-day deposit rule and future PPF rate changes.

PPF Account Interest Calculator – Manual Method

If you prefer a simple manual estimate, here is a beginner-friendly way to understand how PPF grows over time.

Example

Investment: ₹1.5 lakh per year (maximum allowed)

Interest rate: 7.1% per year

Tenure: 15 years

If you invest ₹1.5 lakh at the beginning of every year (following the 5th-day interest rule), the approximate result after 15 years would be:

| Item | Approx Value |

|---|---|

| Total invested | ₹22.5 lakh |

| Interest earned | ~₹18.2 lakh |

| Maturity amount | ~₹40–41 lakh |

This is only a planning estimate. The actual maturity value may vary because PPF interest rates can change periodically, and deposits made after the 5th of a month may reduce that month’s interest. To understand whether this growth is enough in real terms, you can also read PPF interest vs inflation.

Tips to Maximise PPF Interest

A few simple habits can improve your PPF interest outcome without increasing risk.

- If investing yearly, deposit before 5 April to capture April’s full interest window.

- For monthly contributions, deposit before the 5th of each month so the amount is counted for that month’s interest.

- After the initial 15-year tenure, extend your PPF in 5-year blocks. Over 25+ years, compounding becomes significantly stronger.

If you are deciding between withdrawal and continuing your investment, you should also understand PPF loan vs withdrawal options.

Final Teacher Insight

In many staffroom discussions, teachers focus only on the PPF interest rate. But the real advantage comes from understanding when interest is calculated. A simple habit—depositing before the 5th of the month—ensures the amount is counted for that month’s interest, which can improve long-term returns through compounding.

In PPF, wealth is not built by how much you invest—but by how consistently and timely you invest.

Disclaimer: This article is for educational purposes only. Returns and examples are illustrative and may vary based on interest rate changes and deposit timing. Please verify details with official sources before making financial decisions.

FAQ On PPF Interest Calculation

How is PPF interest calculated—monthly or yearly?

PPF interest is calculated monthly (on the lowest balance between the 5th and last day) but credited once yearly on 31st March.

Will PPF Interest Be Taxable?

No, interest earned on a Public Provident Fund (PPF) account is completely tax-free.

How Is PPF Interest Calculated in Post Office?

Interest on a Public Provident Fund (PPF) account in the post office is calculated monthly on the lowest balance between the 5th and last day of each month and credited once yearly (31st March), as per rules set by the Ministry of Finance.

PPF Interest Calculation Date: When Is Interest Calculated and Credited?

Interest on a Public Provident Fund (PPF) is calculated every month on the lowest balance between the 5th and last day, and the total interest is credited once yearly on 31st March, as per the Ministry of Finance.

How PPF Interest Is Calculated

In a Public Provident Fund (PPF) account, interest is calculated like this:

- Every month, the bank or post office checks your lowest balance between the 5th and the last day of the month

- Interest for that month is calculated on this amount

- All monthly interest is added together and credited on 31st March (as per Ministry of Finance rules)

If you deposit ₹50,000 on 3rd April → you will earn full interest for April but If you deposit on 6th April → you will not earn interest for April

Simple rule:

- Deposit before the 5th = full interest

- Deposit after the 5th = no interest for that month