Table of Contents

TogglePublic Provident Fund (PPF) Guide 2026: Interest, Rules & Tax Benefits for Teachers

Last week in the staffroom, a colleague asked me quietly:

“Sir, PPF safe toh hai… but does it actually create real wealth?”

That question matters more than most people realise.

Because the truth is uncomfortable:

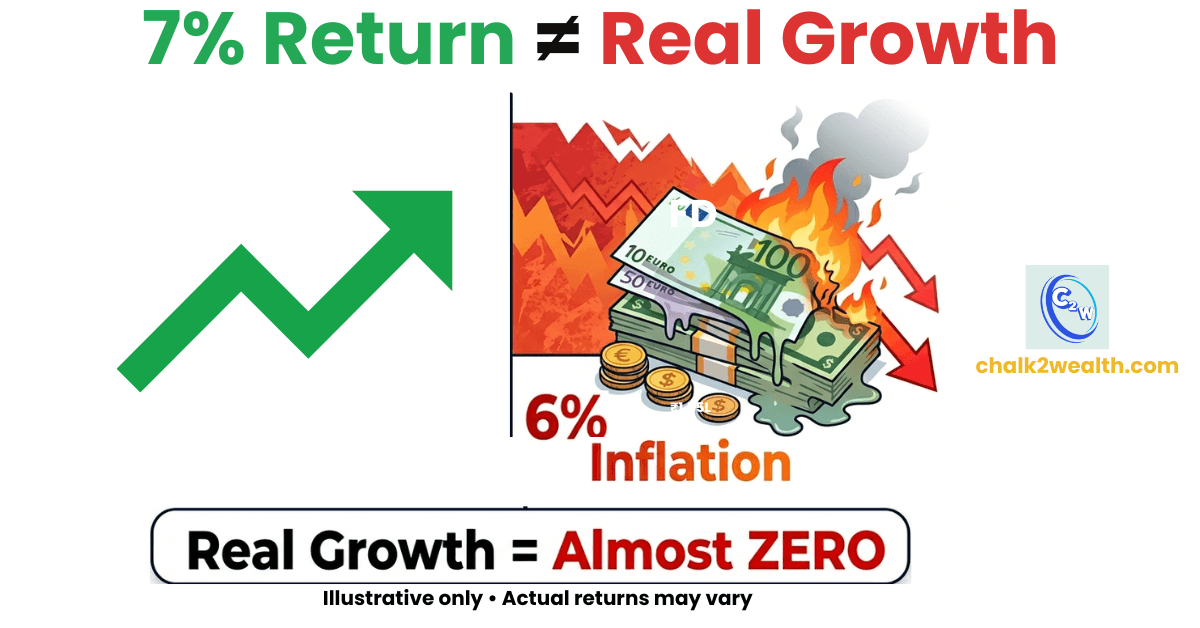

If your return is close to inflation, your money is only growing on paper—not in real life (See our PPF Interest vs Inflation: Is Your Money Still Growing in 2026–27? ) You save for years… but your purchasing power barely moves. This is where most teachers go wrong.

We invest regularly.

We trust the system.

But we never ask if we are using PPF correctly.

In this guide, you’ll understand Public Provident Fund (PPF) not just as a tax-saving scheme, but as a real wealth tool as defined in the official Government small savings scheme guidelines.

- How interest actually works

- Which rules matter most

- When PPF works… and when it doesn’t

Because the goal is not just safety — it’s safe money that actually grows.

Let’s start with the basics.

What is Public Provident Fund (PPF)?

Public Provident Fund (PPF) is a government-backed savings scheme in India that offers tax-free returns, a 15-year lock-in period, and stable interest for long-term wealth creation.

Public Provident Fund (PPF): How It Works & Why It Matters

Public Provident Fund (PPF) is a government-backed savings scheme designed for long-term, risk-free wealth building. It offers tax-free returns, currently around 7.1% (reviewed quarterly), and encourages disciplined investing through a 15-year lock-in period. You can invest between ₹500 and ₹1.5 lakh annually, making it suitable for salaried individuals like teachers who prefer stability over market risk. To maximise returns, deposits should ideally be made before the 5th of each month or as a lump sum early in the financial year (learn the strategy in PPF Interest 2026: The 5th April Trick Every Teacher Must Know). While withdrawals are restricted, this structure helps build consistent wealth over time—explore the detailed guide to understand how to use PPF effectively.

Public Provident Fund Interest: The Small Timing Mistake That Silently Cuts Your Returns

PPF interest is designed to reward consistency, not timing luck—but understanding how it works can quietly improve your returns. The government sets the interest rate (currently around 7.1%), and it is calculated every month on the lowest balance between the 5th and the last day, then credited once a year.

This creates a simple but powerful rule: your money must be in the account before the 5th to earn interest for that entire month. If you deposit after the 5th, you lose one month of growth—every single time. Over 15 years, this small delay can reduce your final corpus without you even noticing.

For teachers, this means discipline matters more than amount. A yearly investment made in early April earns interest for 12 months, while delayed deposits reduce compounding. Even monthly contributions should ideally be automated before the 5th to avoid missing this window.

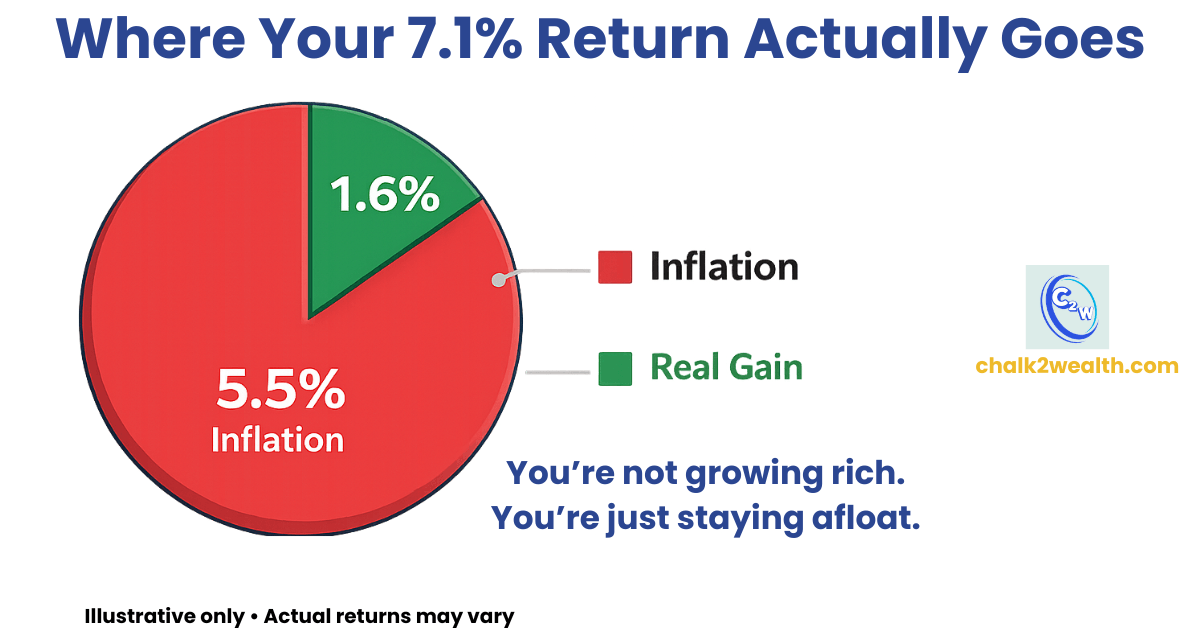

Another key point: PPF interest usually stays slightly above inflation, helping your savings grow in real terms—but the margin is not very high. So the real benefit comes from long-term compounding and tax-free growth, not short-term gains.

In simple terms, PPF rewards three habits: invest early, stay consistent, and avoid withdrawals.

If you want to fully understand how to apply these rules step-by-step, explore our detailed guide on PPF Interest Calculation (2026): Formula, Interest Date & PPF Calculator Explained.

Public Provident Fund Rules: The 3 Decisions That Can Make or Break Your Returns

1. Withdrawal: When and How to Use It

PPF is a long-term scheme, but it does allow partial access. You can withdraw money only after completing 5 financial years (from the end of the opening year). The amount is limited—usually up to 50% of your eligible balance, and only once per year (See our PPF Rules for Withdrawal (2026): How & When You Can Withdraw Your Money Safely.)

For a teacher, this means withdrawals should be used for planned, meaningful goals—like a child’s education, medical needs, or major family expenses. Avoid frequent withdrawals, because every amount you take out reduces your compounding. Think of it as a mid-term support tool, not regular income.

2. Loan: Use Early, Repay Smartly

A PPF loan is available between the 3rd and 5th year of your account. You can borrow up to 25% of your balance, and the interest charged is just slightly above the PPF rate. The key condition: it must be repaid within 36 months –see PPF Loan vs PPF Withdrawal: Which Is Better & When to Choose Each for a clear comparison.

Here’s the practical rule:

Use a loan for short-term needs (emergency expenses, temporary cash gap)

Only take it if you are confident about repayment

Why? Because a loan is reversible—you repay it, and your savings continue growing. This makes it smarter than withdrawal in the early years.

3. Extension: What to Do After 15 Years

After 15 years, your PPF doesn’t stop—you get choices. You can:

Withdraw the full amount (tax-free)

Extend in 5-year blocks with contributions

Or continue without adding money (learn the options in PPF Extension Rules 2026: What Investors Should Do After 15-Year Maturity

If you still want safe, tax-free growth, extending with contributions is powerful. If you need flexibility, continue without deposits and withdraw when required.

PPF is not restrictive—it’s structured. Once you understand these rules, you can use it intelligently without breaking long-term growth.

For deeper clarity on calculations and timing, read PPF Interest Calculation (2026): Formula, Interest Date & PPF Calculator Explained

PPF Tax Benefits: Why You Keep More of What You Earn

Most people think PPF gives “safe returns.”

But here’s the real truth: PPF doesn’t just grow your money—it protects it from tax at every stage.

First, under Section 80C, you can invest up to ₹1.5 lakh per year and reduce your taxable income. That means immediate tax saving—something most teachers actively need while managing monthly budgets.

But the real power is hidden in one simple concept: EEE (Exempt–Exempt–Exempt)

- You invest → No tax (deduction under 80C)

- Your interest grows every year → No tax at all

- You withdraw after years → Still no tax

Even partial withdrawals during the journey are completely tax-free under current rules

Now compare this with fixed deposits—where interest is taxed every year—and you’ll realise something shocking:

In many cases, PPF’s “7.1% tax-free” can beat higher taxable returns.

But many investors still worry—can this tax-free benefit change in future?

Get the clear answer in Is PPF Withdrawal Taxable from 2026? What Every Teacher Must Know.

For conservative investors, this means peace of mind—your money grows steadily, safely, and most importantly, without being eaten away by taxes over time.

2026 Reality Check: New Tax Regime vs PPF

As of the 2026-27 Budget, most teachers are now under the New Tax Regime. You might be wondering: “If I don’t get the ₹1.5 Lakh deduction (Section 80C) anymore, is PPF useless?”

The answer is a big NO. Here is why:

- The “Double Exempt” Advantage: While you don’t get a deduction on the investment in the New Regime, the Interest earned and the Maturity amount remain 100% tax-free.

- PPF vs. Fixed Deposits: In 2026, bank FD interest is fully taxable. If you are in the 20% or 30% tax bracket, a “7% FD” actually only gives you about 4.9% to 5.6% after tax.

- The Verdict: Even without 80C, PPF’s tax-free compounding still beats almost every other “safe” debt instrument in India. It’s not just about saving tax today; it’s about not paying tax on your wealth tomorrow.

Public Provident Fund (PPF) vs FD, SIP & NPS: Which Actually Builds Real Wealth?

| Feature | PPF (Public Provident Fund) | Bank Fixed Deposit (FD) | Equity SIP (Mutual Funds) |

| Risk Level | Zero (Govt. Backed) | Low (Bank Guarantee) | Moderate to High |

| 2026 Returns | 7.1% (Fixed) | 6.5% – 7.5% (Variable) | 12% – 15% (Estimated) |

| Tax on Returns | 100% Tax-Free (EEE) | Fully Taxable | Taxable (above ₹1.25L) |

| Effective Return | 7.1% | ~5% (After 30% Tax) | ~11-13% (After Tax) |

| Lock-in Period | 15 Years | No (but penalty applies) | No (Liquid) |

| Best For… | Safe Pension Base | Emergency Fund | Wealth Multiplication |

PPF offers ~7.1% completely tax-free (EEE), FD gives ~6–7% but interest is taxable, while SIPs may deliver 10–12% over the long term—where gains above ₹1.25 lakh per year are taxed (LTCG). The real difference is what remains in your pocket after tax.

Most teachers believe one thing: “Safe = enough.”

But here’s the uncomfortable truth: choosing the wrong “safe” option can quietly cost you lakhs over time.

1. PPF vs Fixed Deposit: Safety vs Silent Tax Loss

Fixed Deposits feel simple—flexible tenure, easy withdrawal, and familiar. But here’s the shock:

FD returns are fully taxable.

So a 6.5% FD can drop to around 4.5–5% after tax. Meanwhile, PPF offers ~7.1% completely tax-free, making it stronger for long-term wealth.

- Risk: Both low

- Return: PPF wins after tax

- Liquidity: FD wins

- Purpose: FD = short-term, PPF = long-term

For a detailed breakdown, read PPF vs Fixed Deposit: Which Is Better for Teachers After Tax?

2. PPF vs SIP: Safety vs Real Growth

PPF gives stability. SIP in Quality mutual Fund gives growth.

Here’s the reality:

PPF protects money, SIP grows it.

PPF returns stay around 7%, while equity SIPs have historically delivered higher long-term returns (with ups and downs).

- Risk: PPF low, SIP market-linked

- Return: SIP higher (long term)

- Tax: PPF fully tax-free, SIP partially taxable

- Purpose: PPF = stability, SIP = inflation-beating growth

Understand this deeper in PPF vs SIP in 2026: Which Investment Will Secure Your Future

3. PPF vs NPS: Control vs Pension Discipline

Both are long-term tools—but very different. PPF gives full control; NPS locks you into retirement structure.

PPF is flexible (withdrawal + extension). NPS pushes you toward pension with market-linked returns.

- Risk: PPF safe, NPS moderate

- Return: NPS higher potential

- Tax: PPF fully tax-free, NPS partly taxable at maturity

- Purpose: PPF = safe corpus, NPS = retirement income

Compare clearly in PPF vs NPS: Which Is Better for Long-Term Retirement Savings for Teachers?

Final Reality Check

No single option is “best.” The smartest teachers don’t choose one—they combine:

- PPF for safety

- SIP/NPS for growth

- FD for short-term needs

Because real wealth is not built by choosing sides—it’s built by balancing safety and growth intelligently.

How to Manage Your Public Provident Fund (PPF) Account Without Losing Returns

Most people open a PPF account… and then forget it.

That’s the biggest mistake—because PPF rewards discipline, not just investment.

First, understand your limits clearly. You must invest at least ₹500 per year to keep the account active, and you can go up to ₹1.5 lakh annually. Anything beyond this earns no interest—so over-investing is a silent loss.

Now comes the real game-changer: timing.

PPF interest is calculated based on the balance before the 5th of each month. So if you deposit after the 5th, you lose one month of interest—every time. Over 15 years, this small delay can quietly reduce your final corpus.

Best strategy:

- Invest a lump sum in April if possible

- Or set a monthly auto-deposit before the 5th

Consistency matters more than amount. Even small, regular deposits can build a strong corpus over time (learn the basics in Investing in PPF: 8 Smart Things to Know Before You Start )

Also, don’t ignore tracking. Many teachers check their balance only at maturity—which is risky. Use net banking or mobile apps to check your PPF balance online regularly(step-by-step in How to Check PPF Balance Online (2026): SBI, Post Office & Banks )

In simple terms: PPF doesn’t need effort—but it demands discipline.

Stay consistent, stay early, and let time quietly build your wealth.

Is Public Provident Fund (PPF) Still a Good Investment in 2026?

Most teachers invest in PPF thinking: safe hai, toh enough hoga.

But here’s the reality—safe doesn’t always mean sufficient.

In 2026, PPF still offers what very few investments can:

- Government-backed safety

- Around 7.1% tax-free return

- Zero market risk

For a salaried teacher, this makes PPF a strong foundation—especially when compared to taxable options. (See the real difference in PPF vs Fixed Deposit: Which Is Better for Teachers After Tax?

But here’s the catch most people ignore: inflation quietly eats your returns.

If inflation stays around 5–6%, your money grows on paper—but in real life, your progress barely moves.. Understand this deeply in PPF Interest vs Inflation: Is Your Money Still Growing in 2026–27?

So how should you think about PPF?

- Good for: safety, tax saving, long-term discipline

- Limited for: wealth creation and inflation-beating growth

If you rely only on PPF, you may feel secure—but your financial progress may remain average. Smart investors don’t reject PPF—they use it correctly. Explore balance in PPF vs SIP in 2026: Which Investment Will Secure Your Future

Final Takeaway

PPF is still a good investment—but only as a base, not the whole plan. Use it for safety. Add growth options for wealth.

How Teachers Should Use Public Provident Fund (PPF) in Their Financial Plan

How Teachers Should Use Public Provident Fund (PPF) in Their Financial Plan

Let me say this clearly—PPF alone will not make you wealthy.

But ignoring PPF is also a mistake.

For teachers, PPF should be your financial backbone, not your entire plan. It gives you what most investments cannot—certainty. No market tension, no tax worries, no sleepless nights. That’s why your first step should always be clarity start here: What Is Public Provident Fund (PPF)? Your Smart Saver Checklist Before Investing

Now the practical strategy:

- Use PPF for long-term goals → retirement, child education

- Invest consistently (even if small) → discipline matters more than amount

- Treat it as untouchable money

But here’s the reality you must accept:

PPF protects wealth—it doesn’t multiply it fast.

So if you stop at PPF, you stay safe… but average. That’s why smart teachers follow a simple mix:

- PPF → safety + tax-free base

- SIP (mutual funds) → growth + inflation protection

This balance is not theory—it’s practical survival in today’s world. You don’t need to take high risk. You just need to avoid one mistake: relying on only one option.

Final Advice

Build your foundation with PPF.

But don’t build your future on PPF alone.